Making a success of Brexit

As Brexit draws closer, Jeremy Bowden takes a look at how exporters are reacting to the prospect of Britain leaving the EU, and what we might expect from a Brexit deal.

With the clock now ticking down the two years to Brexit, UK-based companies will soon find themselves in a very much smaller domestic market. How much of a difference that will make is highly uncertain at this stage. Above all, it’s difficult to tell whether recent comments from EU representatives are realistic, or simply aimed at scaring the UK electorate in the run up to the upcoming general election. If we are to believe the current UK government (at the time of going to print, the Conservative Party), there is nothing to worry about, and its position based on the most open trade arrangements possible: zero tariffs and some control over movement, will win out.

The UK’s decision to leave the EU has, however, produced a number of immediate effects, notably on exchange rates. It has also resulted in a rise in uncertainty, related to whether or not the UK will remain in the single market and a number of longer-term risks including UK policy adjustments, introduction of cross border regulations and the possibility of further breakup of the EU or UK – although the former looks less likely following recent European election results.

Currency ups and downs

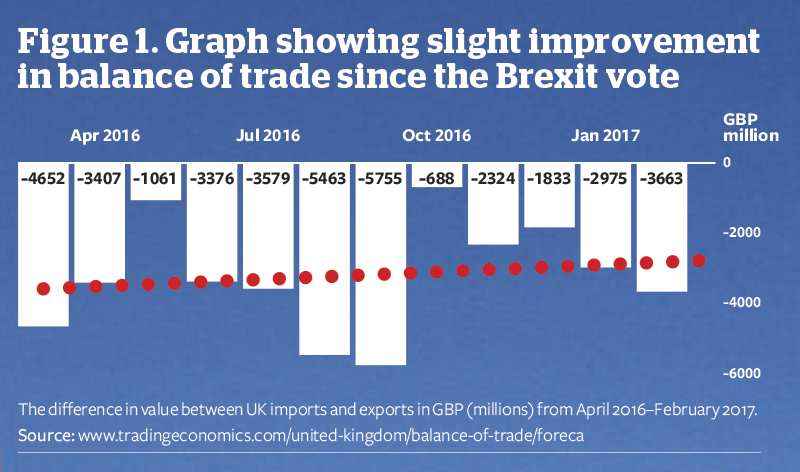

So far, the exchange rate movement has been the most significant Brexit consequence. If it’s permanent, as looks possible, this will improve exporters’ competitive position by reducing prices relative to overseas competitors – boosting exports and making imports less competitive. When combined with the government’s new industrial strategy, which is intended to boost exports and narrow the trade deficit (see Figure 1). However, any exporters with significant reliance on imported raw materials or components have seen costs rise, forcing them to raise prices, which has countered the exchange rate advantage for some.

In the North Sea, most costs are in dollars, so it has become relatively cheaper to invest there since the pound fell after the referendum result. For example, the cost of developing Premier Oil’s Catcher field was originally set at a rate of US$1.60 to the pound. That’s been lowered to US$1.31, representing about US$100m of savings on the project.

Areas like nuclear development, where most investors are based overseas, may also be affected by the forex move, with Hinkley Point C likely to see another rise in sterling estimated costs. However, once again, the weaker pound makes UK-sourced inputs relatively more competitive.

Looking further ahead, a rise in import tariffs resulting from Brexit could offset any exchange rate advantage, hitting exports to the EU, although it could help domestic suppliers expand local market share in areas where competition from imports is high. If there is failure to reach a Brexit agreement, World Trade Organization (WTO) rules will apply, and that means tariffs of around 10% on most manufactured goods. On 30 April Theresa May repeated her belief that ‘no deal would be better than a bad deal’, reminding us that WTO rules are perhaps a real possibility – although this, as with recent comments from EU leaders, could be early posturing in the negotiations process.

WTO rules could mean further instability for the pound – but also for the euro, with the UK being Europe’s biggest single trading partner. Britain’s substantial trade deficit with Europe means European exporters would be hit hard by WTO rules.

There are also a number of uncertainties that arise as a result of Brexit related to interconnector trade (electricity and natural gas cross border trade between the UK and EU) and clean energy policies. The extent of the impact will depend on whether any agreement to leave will be aimed at maintaining maximum cooperation, along with how closely the UK follows EU energy and climate policy. There had been speculation that the UK might reverse key laws and practices – such as emissions goals or other elements of environmental policy – although there is little sign of that so far.

Inward investment in the UK energy sector may also be hit during the run up to a deal, as higher returns are required to compensate investors for the uncertainty. This puts upwards pressure on the cost of financing, raising the cost of investment in the UK energy sector. The scale of planned infrastructure investment in the electricity sector over the next decade means that even small increases in the cost of financing could have large consequences for total investment costs.

Brexit uncertainty reduces investment activity; some growth with more distant markets

The UK investment community has its sights fixed firmly beyond Europe according to a new report by BusinessesForSale.com, although activity is down overall on heightened uncertainty over Brexit. The report, which examines the online activity of British investors in comparison to those overseas, has made the following discoveries:

- UK investors’ interest in UK businesses has dropped by 9.8%

- UK investors’ interest in European business has fallen in every European economic country surveyed, peaking at a 37.45% decline in Belgium, with France falling by 32.94%, Germany by 30.04% and Ireland 30.04%

- UK investors’ interest has grown the most in Australia and Japan with growths of 81.6% and 67.72%, respectively

There were also signs of the wider world showing more interest in investing back in the UK:

- Investors in the UK from the US were the highest in volume and increased by 11.56%

- Investors from Australia were second in terms of volume, and rose by 79.06%

- The volume of visitors from Asian countries remained lower overall, but increased substantially in percentage terms: Japan by 207.14%, Singapore by 55.59%, Hong Kong by 33.39%

The figures cited compare the period from 12 March to 14 April for 2016–17, with that of 2016–17 and so cover the Brexit referendum results, but not the announcement of the UK general election, which is predicted to bring more uncertainty to the market.

Routes out of Europe

Post Brexit options include the halfway house of the European Economic Area (EEA), which is the option Norway has settled for. This would involve more or less automatic acceptance of all the energy and trade rules decided in Brussels. Another alternative is the Swiss model, which would exempt the UK from EU competition law and state aid rules, leaving energy arrangements with the EU to be worked out on a case-by-case basis.

Or the UK could manage to negotiate a unique arrangement unlike either Norway or Switzerland’s. That appears to be the objective of the current UK government and the main opposition, the Labour Party, both of which have said they favour a free trade deal negotiated very similar to current arrangements, alongside leaving negotiations, with some limits on freedom of movement.

Ana Stani, partner at E&A Law Ltd, said her company was working on various scenarios for UK and EU members, commenting that, ‘Although the existing models [Norway and Switzerland] are unlikely to fit. Freedom of movement and access to the single market seem unresolvable, and given this stance it looks like they might not be able to agree on anything, but I suspect this may change.’

'On nuclear the main issue is state aid, so if the UK did not choose the Norwegian model, it would not have to comply with state aid rules, so the UK could raise the price it pays for nuclear even further... I doubt [the new government] would want to do that with Hinkley Point C, but it may free the government’s hand with respect to new developments, depending on the deal done.’ said Ms Stani.

She said it was single market issues, such as around trading and tax rules, the freedom of establishment, and the freedom of movement of people and capital that could have an impact on companies’ bottom lines. ‘Companies need to decide on possible scenarios and decide what to do in each eventuality,’ she added.

Put trade first

The best way to reassure the UK’s energy supply chain and reduce uncertainty is for the government to provide barrier-free relationships and access to the EU markets, with low or no tariffs, and minimal customs processes – very much in line with current government and main opposition’s apparent thinking, but conditional on EU agreement.

A clear regulatory plan to give continuity and facilitate ease of trade is also a key goal, along with a migration system that enables business to retain access to key EU workers and skills, and protect access to EU R&D and innovation funding. There is also concern that without a smooth transition over the next two years and beyond, the risk of underinvestment will grow as uncertainty builds.

At this stage, it looks questionable whether all these conditions will be achieved, with the UK apparently prepared to accept no deal and EU members unanimously refusing to even negotiate on trade matters until after divorce arrangements are finalised. Exiting the single market appears a real possibility, which could make it difficult to achieve ‘barrier free relationships and access to EU markets’. On the other hand, the UK’s clout in EU trade is substantial and it may be that a mutually acceptable, and exceptional, deal still wins out. Whatever the outcome, there will be advantages and disadvantages from Brexit – those companies that use the advantages and offset the disadvantages will be best placed. The prospect already appears to be refocusing investors around the world, helping with the push towards a wider global trade focus (see box), supported by groups such as UK Export Finance, which works with 70 private credit insurers and lenders to ensure export opportunities are funded.

Follow us

Advertise

Free e-Newsletter