Special report: From Cop26 to Ukraine: The ever-changing dynamics of the energy sector

As short-term pressures on energy security and affordability begin to mount, Tom Wadlow asks, what does this mean for the energy transition and net zero?

It is hard to keep energy away from the news at the moment. The current volatility in the energy market is being felt far and wide. Consumers are facing the reality of rising gas and electricity bills, while businesses across all sectors are struggling to operate at a profit while suffering higher overheads.

What we are currently witnessing cannot be attributed to a single event. The COVID-19 pandemic brought entire economies to a standstill for the best part of two years and disrupted normal supply and demand patterns, while, following commitments made at COP26 in Glasgow, energy transition policies are gathering momentum and will be put under the spotlight once more with the upcoming COP27 conference in Egypt.

Meanwhile, supply chain challenges around transportation, transmission and storage infrastructure have been issues for years and are finally being brought into sharp focus as the world wakes up to what ‘energy security’ truly means.

“Some of the biggest supply chain challenges impacting the energy sector should come as no surprise, as the sector has a long history of insecure supply chains due to geographic resource concentrations,” comments Margaret Kidd, Programme Director and Instructional Assistant Professor in supply chain and logistics technology at the University of Houston.

From one crisis to another

All of this is without mentioning the current crisis in Ukraine. “Substantive challenges are playing out globally at multiple scales,” says Kidd. “Regionally, Europe’s move to decouple from Russian fossil fuel supplies begins with diversifying supply sources, along with committing to time-critical infrastructure investment such as the expansion of infrastructure capacity in terms of liquefied natural gas (LNG) import terminal capacity and regional gas hubs, and connectivity of North African gas pipelines beyond Spain to central Europe.”

The war in Ukraine is already beginning to make its mark on the energy landscape, which begs the questions: how far will the impacts go, and how long will they last?

“In the short-term, steps taken by the countries to reduce or eliminate their purchase of Russian oil and gas will cause economic hardship for many consumers,” says Steve Crolius, President of Carbon Neutral Consulting and a former climate adviser at the Clinton Foundation.

“The price will remain elevated until supply goes back up or demand goes down. Since global demand for energy tends to increase steadily over time, prices in the petroleum market will remain elevated until either Russian oil and gas is reintegrated into the global supply picture, other oil and gas-producing nations increase their rate of production, or alternative sources of energy can be brought online in sufficient quantity.”

Europe’s move to decouple from Russian fossil fuel supplies begins with diversifying supply sources, along with committing to time-critical infrastructure investment Margaret Kidd, Programme Director, Supply Chain, University of Houston

In Crolius’s view, these prospects could drag on for years, meaning cost challenges are likely to remain for the foreseeable future without a realistic quick fix. Indeed, sustainable energy systems cannot be built at such a pace that they will meaningfully affect short-term prices.

What does this mean for the energy transition?

One of the most intriguing questions arising from the current situation is what impact recent events will have on the energy transition and net-zero agenda. While the pandemic may have contributed to a rise in conscious consumption, and sustainability awareness being higher than ever, the Ukraine crisis has exposed the vulnerability of nations that do not produce substantial proportions of their own energy. Are we now looking at a trade-off between sustainability and security? Between cost and climate change?

For Stuart Broadley, CEO of the EIC, key questions remain unanswered. “Clearly, the priority is energy security today, almost at any cost,” he says, “and this follows a period of prioritisation on energy transition – again, almost at any cost. No one has answered the question ‘what is the most affordable and cheapest way to achieve net zero?’, and no one seems able to answer what the cheapest way of mitigating the risk of losing Russian oil and gas into Europe is either. Urgency is trumping economics in each case.

“Do I think this will come back to bite us? Absolutely, yes. Affordability, the third leg of the energy trilemma, is long overdue to be considered the priority, but so far is it the lonely laggard.”

Broadley is involved with energy sector innovators and holds conversations with key protagonists on a near-daily basis.

There are also serious puzzles to be solved at a strategic level; from a technological standpoint, the market has never been in a better position to push the energy transition agenda forwards in a way that can tick the long-term security and affordability boxes.

“This is a market like no other that I have seen, where all technologies are booming, all at the same time, and the latest announcements about the UK energy security strategy following the Russian invasion of Ukraine have only exacerbated this further,” Broadley says.

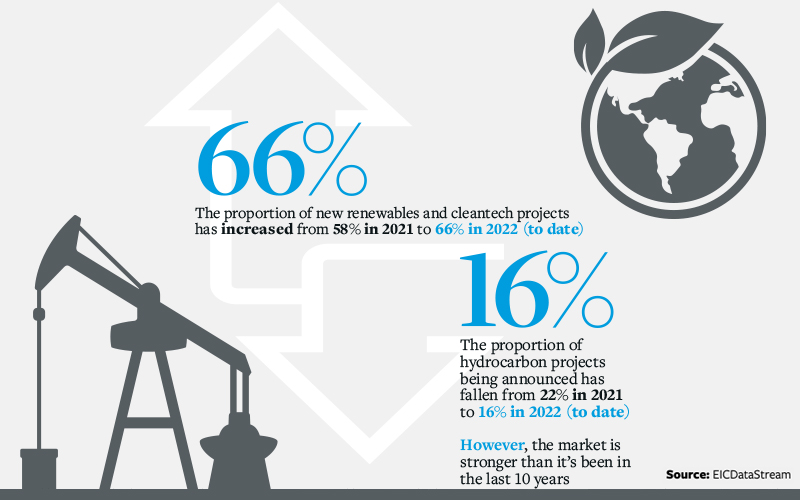

“Furthermore, our global data shows that the proportion of energy projects being announced that are cleantech and renewables-focused has increased from 58% in 2021 to 66% in 2022 so far. Meanwhile, the proportion of project announcements involving mature hydrocarbons has fallen from 22% to 16%.

“However, traditional hydrocarbon markets are stronger than they have been for 10 years as markets struggle to account for the planned and unplanned loss of Russian oil and gas to Europe. And new technologies like hydrogen and carbon capture are being accelerated even faster – again as a defence against premature loss of gas into the system.”

Indeed, the UK government has announced plans for up to 95% of its electricity to come from low-carbon sources by 2030. Central to its new energy security strategy is the construction of eight new nuclear reactors, which will be supported by onshore and offshore wind, solar, and a targeted doubling of planned hydrogen output.

The elephant in the room, as far as the UK is concerned, is fracking. “Although the government will likely bend to political pressure to re-open apparent consideration for fracking, a key issue will be whether it passes the local community buy-in test,” says Broadley.

“This is also why the government may be hesitant to sign off on the large-scale reintroduction of onshore wind, preferring offshore wind instead. However, it appears that the use of some onshore wind is on the table, at least for the time being.”

Elsewhere, LNG has been identified as the cleanest fossil fuel that can aid energy transition and replace Russian supplies. EIC data shows that several EU countries appear to be betting on floating offshore LNG terminals to raise their import capacity. In Germany, the first of several terminals is due to come online before the end of the year, while Italy and the Netherlands are also making moves that will bring Europe more in line with other global regions, which have so far been more receptive to floating storage and regasification units.

This is a market like no other that I have seen, where all technologies are booming, all at the same time, and the latest announcements about the UK energy security strategy following the Russian invasion of Ukraine have only exacerbated this further Stuart Broadley, CEO, EIC

Of course, energy transition relies on the availability of an abundance of resources, including a series of critical minerals that are also subject to acute supply challenges.

“Price fluctuations for minerals such as lithium, cobalt, copper and nickel call for a permanent intergovernmental organisation, similar to OPEC, to co-ordinate and unify mineral policies among member countries to secure fair and stable prices for producers,” Kidd says.

“This could enable an efficient, economic and regular supply of these minerals to consuming nations, a fair return on capital to stakeholders investing in the industry, and global standards for sourcing and social responsibilities to nations where these extractive activities are occurring. Additionally, western countries must expand capabilities for manufacturing, processing and refining of critical minerals, as capacity is highly concentrated in China.”

The longer-term

Looking ahead, although there are sizeable barriers to energy transition, such as the immediate need for energy security and numerous supply chain constraints, failure to drive the agenda forwards now could carry enormous long-term consequences, says Crolius.

“I believe that failure to address the climate crisis in an effective and timely manner will cause an amount of human hardship that will dwarf that being experienced in Ukraine, as horrific as that is,” he says. “Therefore, the better course would be to prioritise investments into sustainable energy systems over efforts to increase fossil fuel production.”

Predicting what the future might look like is, of course, riddled with challenges. Here, up-to-date data and factual insight offers the best form of grounding for both governments and enterprises to base their strategies on.

“The EIC continues to stay abreast of the rapidly-moving picture thanks to our extensive databases and networking capabilities that bring together key stakeholders all around the world on a regular basis,” Broadley says.

“By being a member, together we can move forwards through these difficult issues in a meaningful way, through positive engagement.”

Indeed, such collaboration will only help to advance critical energy transition progress. Here, Crolius predicts that, during the course of this century, a global sustainable energy system will substantially take the place of the legacy fossil energy system – with the world being somewhere in the middle of the process by the time the 2050 net-zero target adopted by the UK and some other nations arrives.

“The faster we can move in this direction, the better for the climate – and the worse for autocratic regimes that are propped up by the export of fossil energy commodities,” he adds.

Broadley agrees that there is no reason to change priorities around net zero, although it may cost more to achieve these ends because of the current urgency to take action.

Sustainable energy systems cannot be built at such a pace that they will meaningfully affect short-term energy prices Steve Crolius, President, Carbon Neutral Consulting

He concludes: “For ‘UK plc’, this is a unique chance to maximise local content – for the UK energy supply chain to stake its claim for the lion’s share of this technology, leveraging its globally recognised track record of quality and innovation, and proactivity to invest heavily in new capacity and capability, backed up by unwavering government policy to ensure UK energy security of supply.

“By seeding and rooting a UK-based energy transition supply chain, the UK would go on to help the rest of the world reach net zero – a world-class supply chain with capability proven in the UK, competitive globally, for decades to come.”

Image credit | Shutterstock | iStock

Follow us

Advertise

Free e-Newsletter