Energy 2025: Policy, markets and the transition ahead

Energy in 2025 was defined by shifting priorities – governments recalibrating policy, investors chasing stability and markets reacting to global tensions and rising demand. Amid disruption and reinvention, what do these forces reveal about the transition ahead as innovation, investment and resilience drive future growth? Jonathan Dyble, Partner, WD Editorial

The outlook for the energy sector was promising ahead of 2025.

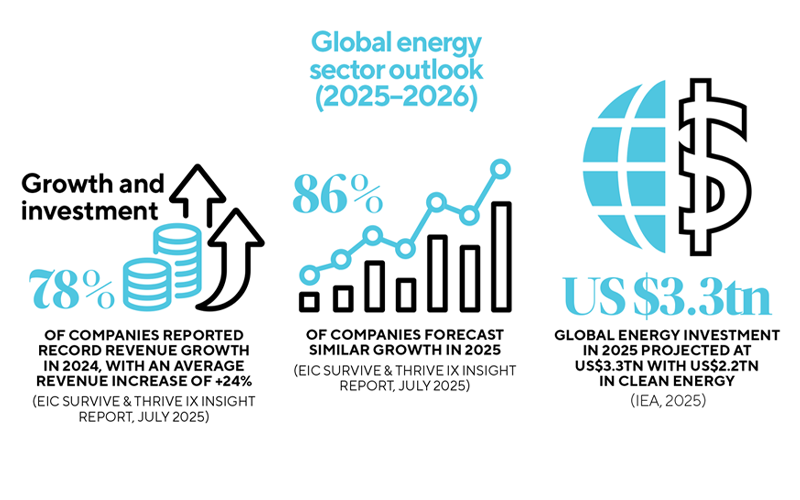

According to EIC’s 2025 Survive & Thrive Report, 78% of companies reported record revenue growth in 2024, with an average increase of 24%. This momentum was expected to continue, with 86% of firms forecasting similar growth this year.

Such optimism was not misplaced. Milestones have been met, with global renewable electricity generation having surpassed coal for the first time in the first half of 2025. Likewise, in June, the International Energy Agency reported that global energy investment for the year would likely hit a record US$3.3tn, with US$2.2tn of this flowing into clean energy.

Behind these headlines, however, challenges have remained. Policy fragmentation, infrastructure bottlenecks and disparities in regional performance have all remained prevalent, and much like any other year, there have been winners and losers. As 2025 draws to a close, we review some of the sector’s defining developments, while offering informed perspectives on the opportunities and risks shaping up in 2026.

Global policy and geopolitical shifts

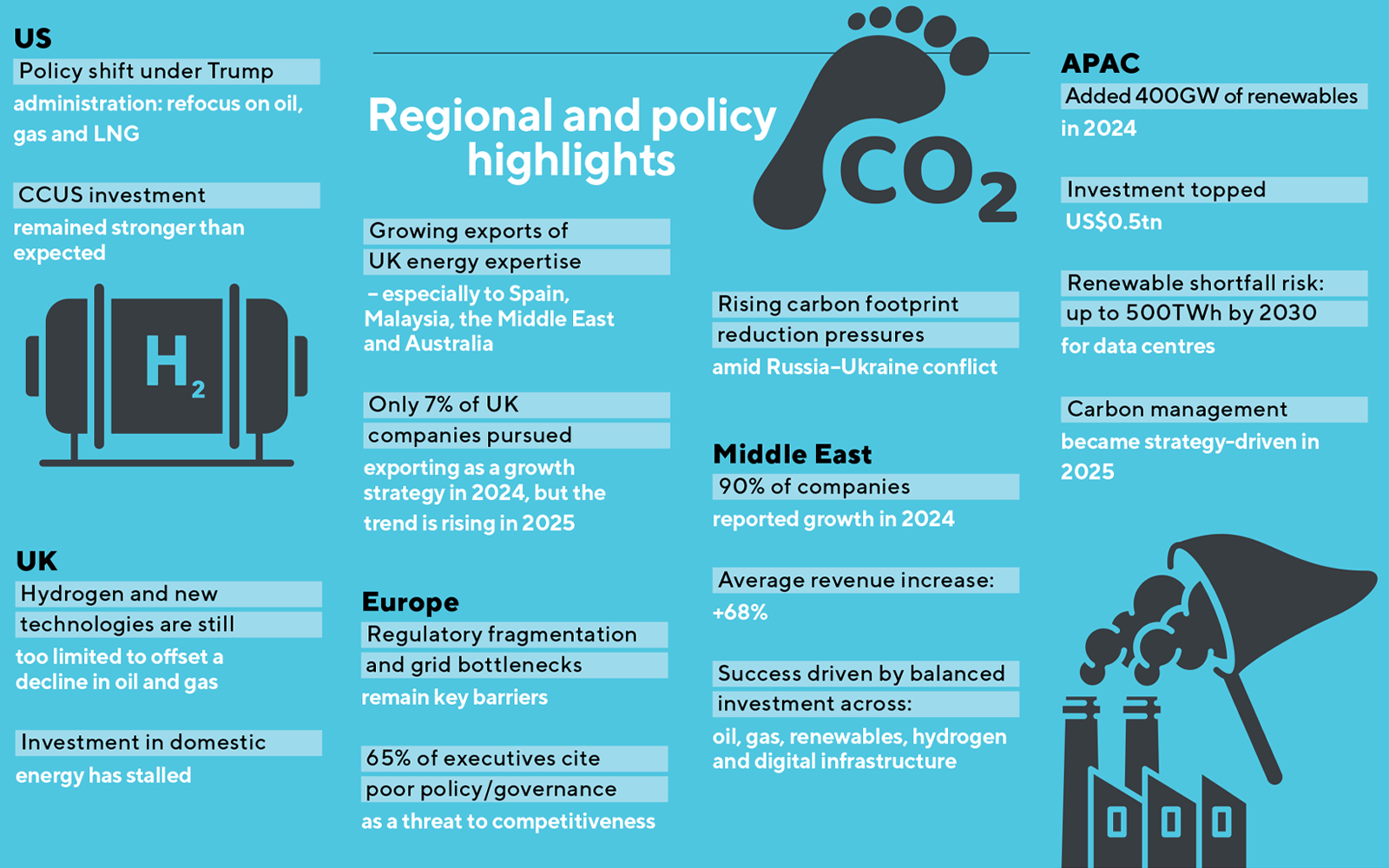

As expected, Donald Trump’s return to the US presidency had a major impact on energy policy and intent.

Rebecca Groundwater, Head of External Affairs at the EIC, says that while the shift in US policy was stark, not all technologies suffered equally. “Obviously in the US we had the significant move away from wind, and a refocus on oil and gas and liquefied natural gas (LNG),” she explains. “But we haven’t seen the drop-off in carbon capture, utilisation and storage (CCUS) that was expected.”

Data centres alone could face a renewable shortfall of up to 500TWh by 2030 Teo Han Yong, GoNetZero

Looking at the UK, she also flags that earlier pivots away from oil and gas are now exposing cracks in the supply chain, highlighting that investment has stalled and that technologies such as hydrogen are still too limited in their development to offset any major decline in traditional energy.

“They are too far away, and at too small a scale, to make a difference and deliver a ‘transition’ in jobs and growth,” she says, pointing out that, as a consequence, some UK companies are looking abroad, with rising interest for UK supply chain expertise in Spain, Malaysia, the Middle East and Australia.

Developing export and international trade strategies in new regions continues to be seen by business leaders as the hardest growth strategy, as outlined in EIC’s Survive & Thrive research, with just 7% of EIC member companies pursuing it as a growth strategy in 2024. It has long been viewed as a difficult route to growth due to the complexity of international compliance and logistics. However, Groundwater believes that a corner may have been turned in some regions in 2025.

“We see UK companies beginning to shift personnel out to the Middle East specifically to work on projects,” she says. “With that said, moving people within Europe is trickier due to the issues with movement of people, work visas and the points systems.”

In Europe, Hans-Michael Kursawe, Principal Adviser at TÜV SÜD Energietechnik GmbH, also believes regulatory fragmentation remains one of the biggest barriers to progress. “Stronger coordination and support from European technical organisations will be essential to reduce complexity, accelerate delivery, and attract investment,” he says, specifically highlighting nuclear energy as an area that could benefit from such coordination.

Asia-Pacific’s (APAC) policy landscape, meanwhile, has also seen significant changes. Teo Han Yong, Head, Renewable Energy Solutions at GoNetZero, states that carbon management has shifted from being compliance-driven to strategy-driven in 2025. “Disclosure standards and supply chain pressures have been the biggest catalysts, driving rapid adoption in Singapore and Australia, while markets like Vietnam and Indonesia have moved more cautiously amid regulatory uncertainty,” he says.

Can other regions learn from the Middle East model?

Clearly, policy has moved in different directions in different geographies, with a mixed impact on financing. “The geopolitical narrative has reduced investment in some areas, increased it in others, but every country is different and many will be getting on with the projects which were underway before announcements,” Groundwater says.

One region that has continued to gather momentum is the Middle East. Indeed, it was a standout performer before 2025. EIC statistics show that 90% of companies in the region reported growth in 2024, with average revenues jumping a whopping 68%.

In the US, we had the significant move away from wind, and a refocus on oil and gas and LNG. But we haven’t seen the drop-off in CCUS that was expected Rebecca Groundwater, EIC

A balanced approach to energy transition has been key to this success. Rather than picking winners, regional companies are investing across the board. More than 90% of EIC member companies in the region are still focused on oil and gas, yet renewables, hydrogen and digital infrastructure are also gaining ground.

Europe, by contrast, has been tackling issues such as mounting infrastructure and grid challenges. Despite strong net-zero commitments, 65% of European executives previously cited poor policy and governance as a threat to competitiveness.

Enter Björn Fagerström, Director of Innovation HUB Sweden for HARTING Technology Group. He explains that the cost of operating and migrating energy technologies in Europe has increased notably, in part due to the limited number of suitable suppliers.

“The market has remained concentrated around major players such as ENEL, E.ON, and EDF,” Fagerström adds. “There’s also mounting pressure to reduce carbon footprints and decreased dependency on gas, especially in light of the Russia-Ukraine situation.”

Digitalisation has played a crucial role in 2025, enabling better utilisation of the grid Björn Fagerström, HARTING Technology Group

It is a similar story in APAC. According to Yong, the region added more than 400GW of renewables last year, with investment topping half a trillion US dollars. However, despite the positives, faster progress is needed.

“Data centres alone could face a renewable shortfall of up to 500TWh by 2030,” Yong warns. “This is why companies are increasingly pairing renewables procurement with complementary solutions like carbon credits and digital traceability to manage their full emissions footprint.”

Energy transition, technology and supply chain trends

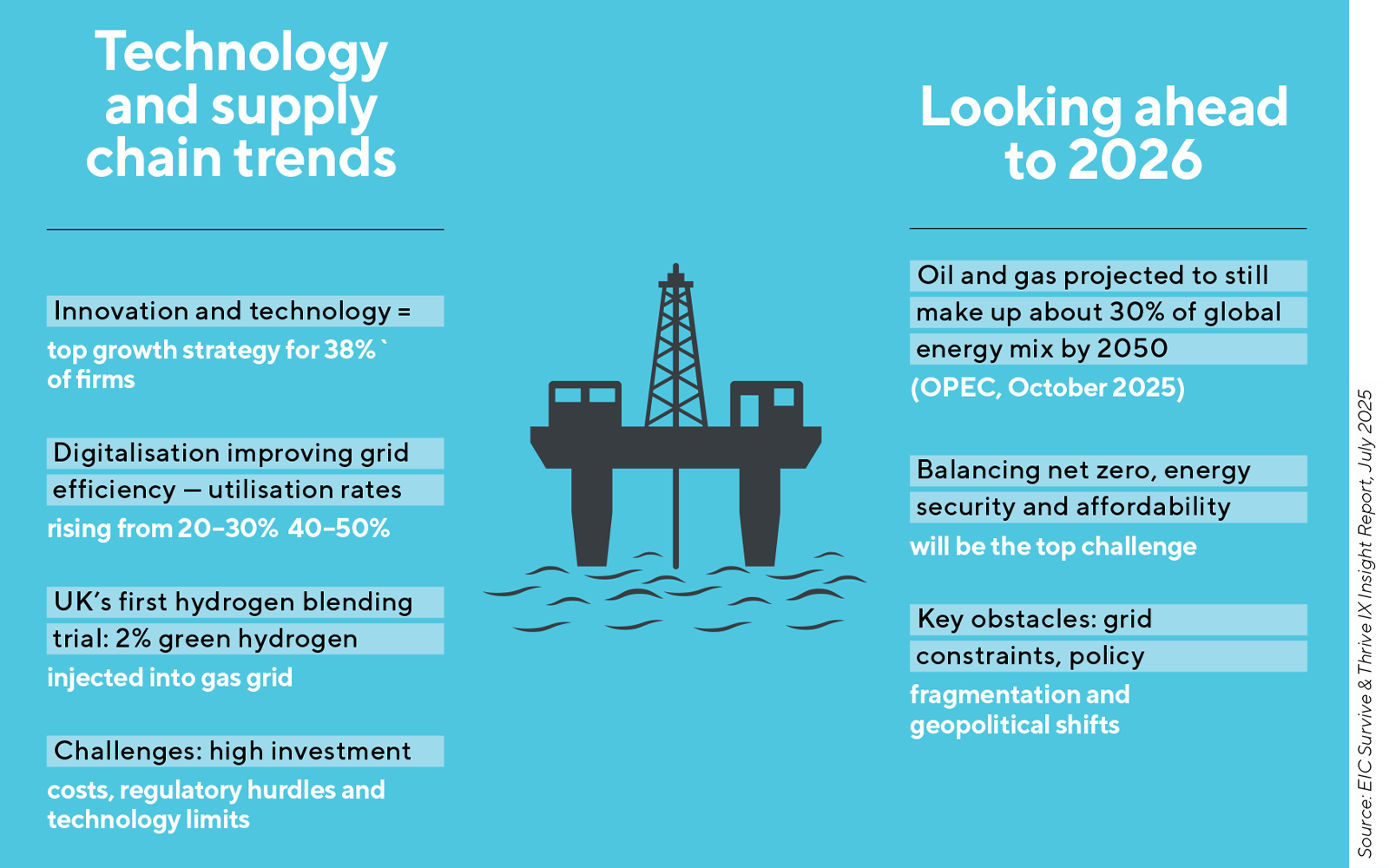

Before the turn of the year, the biggest growth strategy among energy supply chain firms was innovation (including AI and technology), cited by 38% of EIC member companies. For Fagerström, those ambitions have largely materialised and will continue to do so.

“Digitalisation has played a crucial role in 2025, enabling better utilisation of the grid,” he says. “The surge in electricity demand from data centres and e-mobility led to power constraints. However, smart use of data and AI-driven solutions will increase grid utilisation rates to increase from 20/30% to 40/50% in the future. These advances have made grid management more efficient and flexible, supporting the growing needs of modern energy infrastructure.”

Other innovations have taken off this year. For example, the UK conducted its first real-world trial of hydrogen blending, with 2% green hydrogen injected into the national gas grid to power a Midlands plant. Yet for Fagerström, renewables growth has been tempered by “technological limitations, the scale of required investments, and regulatory challenges” in 2025.

Stronger coordination and support from European technical organisations will be essential to reduce complexity, accelerate delivery and attract investment Hans-Michael Kursawe, TÜV SÜD Energietechnik

With renewables arguably stuttering, there have been growing calls to use the Middle Eastern model of balancing investments in clean and traditional fuels. Indeed, the OPEC general secretary warned that oil and gas will still contribute approximately 30% of the global energy mix through 2050, calling for more investment.

In this sense, while we are set to see record investment in energy and clean energy, the dial may well shift again this year.

From grid bottlenecks and regulatory fragmentation to geopolitical curveballs, many hurdles still need to be overcome while balancing competing industry objectives. Energy transition remains a long-term aim. Yet power demands, energy affordability and energy security cannot be ignored at the expense of net zero.

Indeed, perhaps the leading challenge in 2026 will be finding the right balance between these varied priorities.

Image credit | iStock | Getty

Follow us

Advertise

Free e-Newsletter