From industrial strenght to strategic resilience: Europe's hydrogen moment

Europe’s electrolyser industry scaled tenfold in five years and kept its promise. The policy system has not. With projects cancelled, capital stalled and China accelerating, the continent’s green hydrogen lead is far more fragile than the targets suggest.

I’ve spent more than two decades in hydrogen – as a development engineer working on fuel cells at GM, as head of the transport and infrastructure division at NOW GmbH in Berlin, as Director of Market Development and Public Affairs at Nel. I’ve watched this industry go from curiosity to credibility, from PowerPoint to gigafactories. What I’m watching now genuinely worries me: Europe is in real danger of giving away a lead that it spent years earning.

Let me explain why, and why there is also reason for carefully calibrated hope.

European electrolyser manufacturers have scaled annual production capacity from 1GW to more than 10GW since 2020. Companies such as Sunfire, thyssenkrupp nucera, John Cockerill, Nel and Topsoe have delivered what most of the world cannot match. They kept their promise. However, less than 1GW is installed and in operation. The policy system has not kept its end of the deal.

What separates ambition from reality here is not hardware. It is the missing policy architecture to turn industrial readiness into market momentum.

Resilience is the argument

In a world of geopolitical instability and weaponised energy, resilience is no longer political language. It is the capacity to keep factories running without depending on hostile actors for critical molecules. More than 95% of Europe’s hydrogen is still fossil-based – most of it imported. Electrolysers are the most direct path out of that dependency.

Refineries alone represent 58% of Europe’s hydrogen demand, with a potential electrolysis capacity of up to 45GW. Ammonia production adds another 20GW. European manufacturers hold around 30% of global electrolyser manufacturing capacity. The green hydrogen value chain could unlock up to €200bn in export value and 1m direct jobs across the EU.

The numbers, though, are difficult to ignore. The European Resilience Alliance (ERA), a CEO-led cross-value-chain initiative, is direct about the situation: despite a massive project pipeline, fewer than 7% of clean hydrogen projects have reached final investment decision (FID). In its latest market monitoring report, the EU’s Agency for the Cooperation of Energy Regulators (ACER) puts installed EU electrolyser capacity at just 308MW, against a 2030 target of 40GW. More than 50 projects have been cancelled in the last 18 months alone. Renewable hydrogen costs around €8/kg, against just over €2/kg for the fossil alternative.

Europe has no shortage of targets. It lacks a regulatory framework to make them real.

Four things that must happen

The ERA’s diagnosis is familiar: fragmented national regulations, overly complex rules for Renewable Fuels of Non-Biological Origin (RFNBO), uncertain infrastructure timelines and, above all, the absence of bankable demand.

Demand must drive production through immediate transposition of the Renewable Energy Directive III (RED III), lead markets in hard-to-abate sectors via Carbon Contracts for Difference, and mandatory clean procurement criteria. The support framework must be simplified because electricity accounts for up to 70% of levelised hydrogen production costs; grid fee relief, long-term carbon-free power purchase agreements and revised RFNBO rules are essential. Private capital must be unlocked through a predictable carbon price under the Emissions Trading System, a state-backed portfolio guarantee mechanism and a dual-auction system linking hydrogen supply and demand. Finally, infrastructure must be treated as a lifeline for an integrated European energy market, with accelerated delivery of Projects of Common Interest, coordinated cross-border planning and long-term visibility on the European Hydrogen Backbone.

None of the following is hypothetical: industrial job losses, capital flight, stranded assets, missed climate targets and defence vulnerabilities as energy dependencies are exploited geopolitically. China is accelerating. Europe needs to respond with equal seriousness.

A signal from Germany

Germany has taken a significant step, with the German Bundesrat passing an updated greenhouse gas reduction quota (the Treibhausgasminderungsquote) that implements RED III in national law. A binding RFNBO sub-quota for the transport sector steps from 1.5% by 2030 to 10% by 2040, backed by a penalty of €14/kg of hydrogen (€120/GJ). Sunfire estimates that this could unlock demand for up to 5GW of electrolyser capacity over the next five years.

Nils Aldag at Sunfire notes that the 2030 level came in lower than the industry had argued for, and that earlier ambition would have been industrially important. Other sectors beyond transport still need to be addressed. But the demand anchor for transport now exists, changing the investment calculus. Twenty-four other Member States now have a template.

Industry has delivered. Germany just helped to build the market. Every month of delay is a project that will not reach FID in time.

Global trends

Hydrogen in a multi-technology race

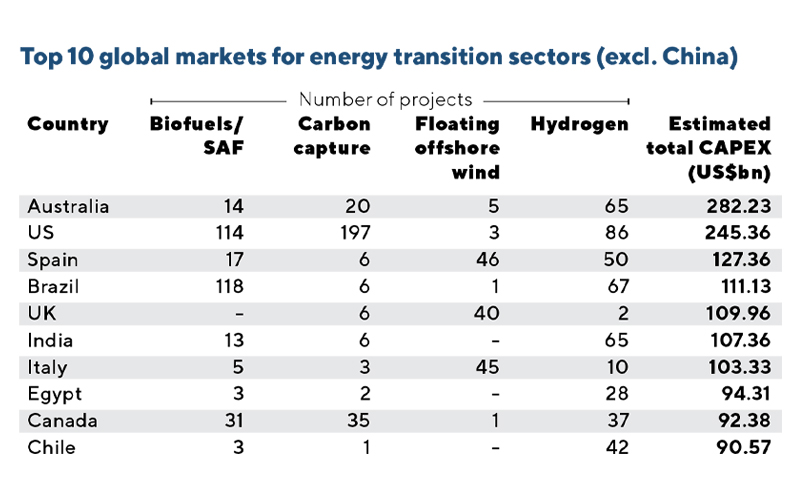

EICDataStream highlights that the energy transition sector continues to attract substantial capital, with total investments reaching US$2.33tn across 2,298 projects focusing on low-carbon fuels and floating offshore wind.

Hydrogen dominates the pipeline at 43.2% (993 projects), followed by carbon capture (22.9%), biofuels and sustainable aviation fuel (SAF) (22.7%) and floating offshore wind (11.2%). Hard-to-abate sectors are the frontier, with clean hydrogen derivative projects targeting steel, chemicals, shipping and aviation. But investment decisions hinge on bankable demand and long-term offtake agreements; projects with secured offtakers are best placed to reach construction.

Robust policy frameworks are proving decisive. SAF mandates, hydrogen/ammonia blending obligations and Contracts for Difference are shaping demand and de-risking projects. In Europe, the Clean Industrial Deal and the Industrial Accelerator Act aim to reduce costs and create markets for low-carbon products. In Asia Pacific, Australia’s Future Made in Australia Act is channelling capital into green metals and renewable hydrogen.

Want to know more about the current state of the Energy transition market? Contact: muhammad.ekrahm@the-eic.com

By Thorsten Herbert, Founder, Hydrogen Now

Image credit | iStock

Follow us

Advertise

Free e-Newsletter