North America leads hydrogen and carbon capture

North America leads in hydrogen and carbon capture investment, Europe shows growing momentum and Asia Pacific trails behind, highlighting how policy and CAPEX shape the global cleantech race By Jack Boggis, Energy Analyst, EIC London

Carbon capture and storage facility during the official opening of the facility at the Boundary Dam Power Station in Estevan, Canada

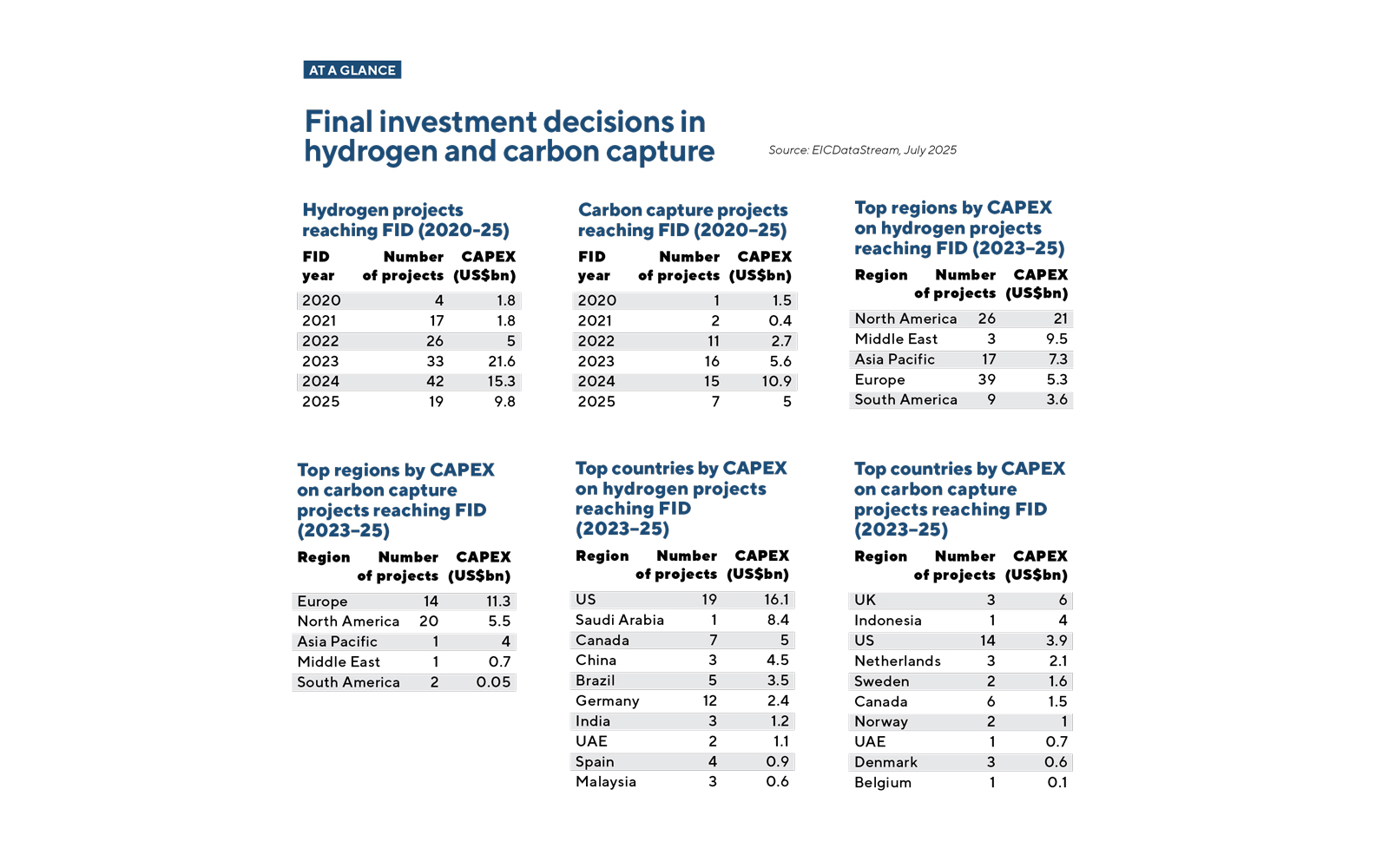

Since 2023, North America has seen 26 hydrogen and 20 carbon capture projects reach a final investment decision (FID), with a combined CAPEX of US$26.5bn, making it the leading region globally.

US policy drives blue hydrogen

The US accounts for 33 hydrogen and carbon capture projects, bolstered by its respective 45V and 45Q tax credits schemes, which have encouraged the development of the cleantech sector through financial incentives.

US president Donald Trump’s One Big Beautiful Bill confirms that the Section 45V clean hydrogen production tax credit will expire in 2028 instead of 2033, while the Section 45Q tax credit remains at US$85 per tonne for point-source carbon capture with geological storage, and US$180 per tonne for direct air capture with geological storage.

Blue hydrogen projects will continue under Section 45Q, but the green hydrogen sector faces cancellations as projects must begin construction by 2028 to secure US$3/kg support. The US is poised to remain a global leader in blue hydrogen development.

Europe’s growing momentum

Europe has seen 53 hydrogen and carbon capture projects reach FID, surpassing North America in project count but having a lower combined CAPEX (US$16.6bn). Germany leads in hydrogen with 12 projects reaching FID, while the UK dominates carbon capture with three projects moving forward, accounting for more than half of Europe’s US$6bn FID projects. The hydrogen sector is still in its infancy, with mostly small-scale projects progressing while larger-scale projects lag behind. In contrast, carbon capture commands higher CAPEX, driven by large storage projects such as HyNet’s Liverpool hub, which aims to capture 10m tonnes of CO₂ annually from 2030.

The US is poised to remain a global leader in blue hydrogen development

Momentum is slowly building in Europe through the second Hydrogen Bank Auction, although the 15 winning projects must reach FID within two and a half years and begin production within five in order to secure funding; most are still in the planning stage.

Asia Pacific faces hurdles

The Asia Pacific region has seen 18 projects reach FID (total CAPEX US$7.3bn), with just one in the carbon capture sector – Indonesia’s US$4bn Vorwata carbon capture, utilisation and storage project. China leads the region, with three hydrogen projects getting the green light. One of these, the US$4bn 640MW Songyuan Hydrogen Energy Industrial Park, has been operating since 2024.

The region is still heavily reliant on fossil fuels and most of the projects moving forward are in the oil and gas sector. Australia is the most progressive country in terms of introducing hydrogen and carbon capture projects, but has seen various cancellations – including its 3GW Central Queensland green hydrogen project – due to high costs, market uncertainty and regulatory hurdles.

Are you ready to export? Email: jack.boggis@the-eic.com

Image credit | Alamy

Follow us

Advertise

Free e-Newsletter