Dual path to energy resilience

Traditional reactors and small modular reactors are enhancing global energy resilience and driving the energy transition, says Firdaus Azman at EIC

Nuclear power is rapidly emerging as an important player in the global shift to carbon-free energy. As the world strives for a cleaner future and better energy security, the relevance of nuclear energy has regained significant momentum, surpassing pre-Chernobyl levels. With renewed governmental support, countries around the world are investing in both traditional nuclear reactors and small modular reactors (SMRs), charting a dual path toward energy resilience and sustainability.

Asia leads the charge

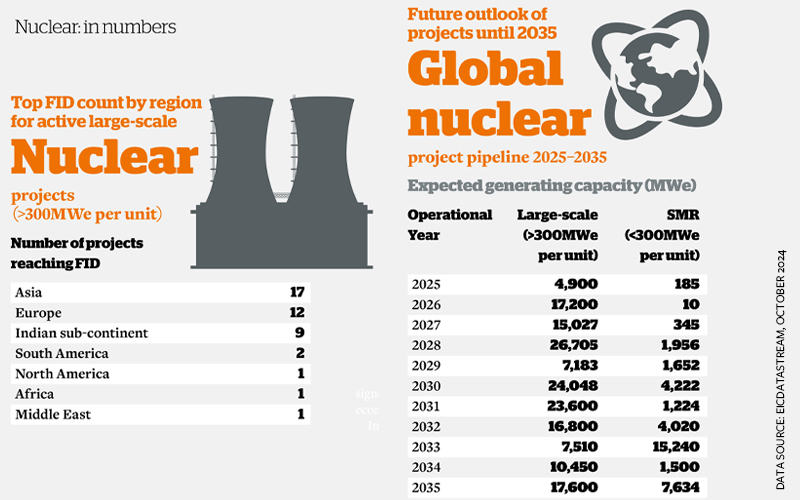

Asia is at the forefront of nuclear expansion, with China and India leading the way in terms of the number of projects reaching final investment decision (FID). These countries, plus South Korea and Japan, have a track record in nuclear power and are using their expertise and supply chains to fast-track new projects.

In Europe, excluding Russia, the drive is equally strong. France, the UK, Czech Republic, Turkiye and Hungary are all advancing ambitious projects that are underpinned by government support and collaboration between public and private stakeholders. These are primarily based on traditional pressurised water reactor technology.

Government support drives expansion

Government policies are pivotal in shaping the progress of nuclear energy projects.

South Korea’s stance on nuclear power has shifted dramatically in recent years. In 2017, President Moon Jae-in made the controversial decision to phase out nuclear energy, but current President Yoon Suk-yeol’s government has reversed this policy. The resumption of major projects, such as the 2.8GW Shin Kori 5 and 6 and the 2.8GW Shin Ulchin 3 and 4 nuclear power plants, signals a strategic shift towards prioritising energy security and economic growth by expanding nuclear power.

In Europe, the focus is on completing major nuclear projects such as the UK’s Hinkley Point C. After years of negotiations, this 3.2GW nuclear power plant is expected to be operational by the end of the 2020s. The path to FID has been lengthy, beginning in 2013 with negotiations between the UK government and the operators, EDF and China General Nuclear (CGN). FID was eventually secured in 2016 after CGN acquired a 33.5% minority stake in the project.

However, the project has faced significant challenges, including escalating costs and delays. Initial cost projections of £18bn in 2016 have ballooned to an estimated £46bn, and CGN halted its funding in December 2023 because of rising UK-China tensions. However, construction has continued despite these hurdles, with notable progress including the arrival of the first of eight steam generators from Framatome in June 2024, and the installation of a 423-tonne steel liner ring in the reactor building in October.

EDF has enlisted the expertise of Assystem, AtkinsRealis, Jacobs and Vulcain Engineering to help in the development of the project. Meanwhile, negotiations between the UK government and EDF are ongoing over a potential loan agreement to address the remaining costs. The UK government remains committed to large-scale nuclear energy, having announced plans for a third nuclear plant at Wylfa and expecting to secure an FID for Sizewell C before the end of 2024.

SMRs: A promising future

Technological advances, particularly SMRs, are reshaping the nuclear energy landscape. These reactors, which have a power capacity of up to 300MWe, are compact and modular, enabling greater adaptability, lower construction costs and better safety compared to traditional reactors. These features have attracted global interest, from established nuclear nations to emerging markets such as Southeast Asia.

EICDataStream projects that SMR deployment will rise steadily from 2027, peaking in 2033. Their factory-based production and the ease with which they can be transported make them particularly suitable for powering energy-intensive operations such as data centres and remote mining facilities, as highlighted in Canada’s SMR roadmap.

While SMRs offer lower upfront costs than traditional large-scale reactors, their nascent stage has limited the number of FIDs. To overcome this, governments and industry stakeholders are pursuing innovative financing strategies, including public-private partnerships to boost investor confidence and accelerate deployment. For example, the UK’s SMR competition, involving companies such as GE Hitachi, Holtec, Rolls-Royce SMR and Westinghouse, shows the potential for collaboration and innovation in this sector.

The road ahead

The future of nuclear power looks promising, with more and more countries recognising its potential to provide reliable low-carbon energy. As technological advances continue and public perception of nuclear improves, we can expect to see a surge in the number of these projects, especially in regions with strong energy demands and concerns about climate change.

By Firdaus Azman, Energy Consultant, EIC

Image credit | iStock

Follow us

Advertise

Free e-Newsletter