Oil and gas projects surge globally

North America, South America and Asia Pacific are driving global oil and gas growth, with liquefied natural gas expansion, offshore projects and midstream investment reinforcing energy security and long-term supply stability By Mariana Messere, Energy Analyst, Eic Rio De Janeiro

The North American oil and gas industry remains a key force in the global energy landscape. The Permian Basin’s resilience and abundant natural gas reserves are reinforcing the region’s strategic importance, with recent geopolitical shifts pushing the narrative from energy transition goals towards energy security and global dominance. North America is the most active region globally in terms of sanctioned oil and gas project development.

North America: Energy security over transition

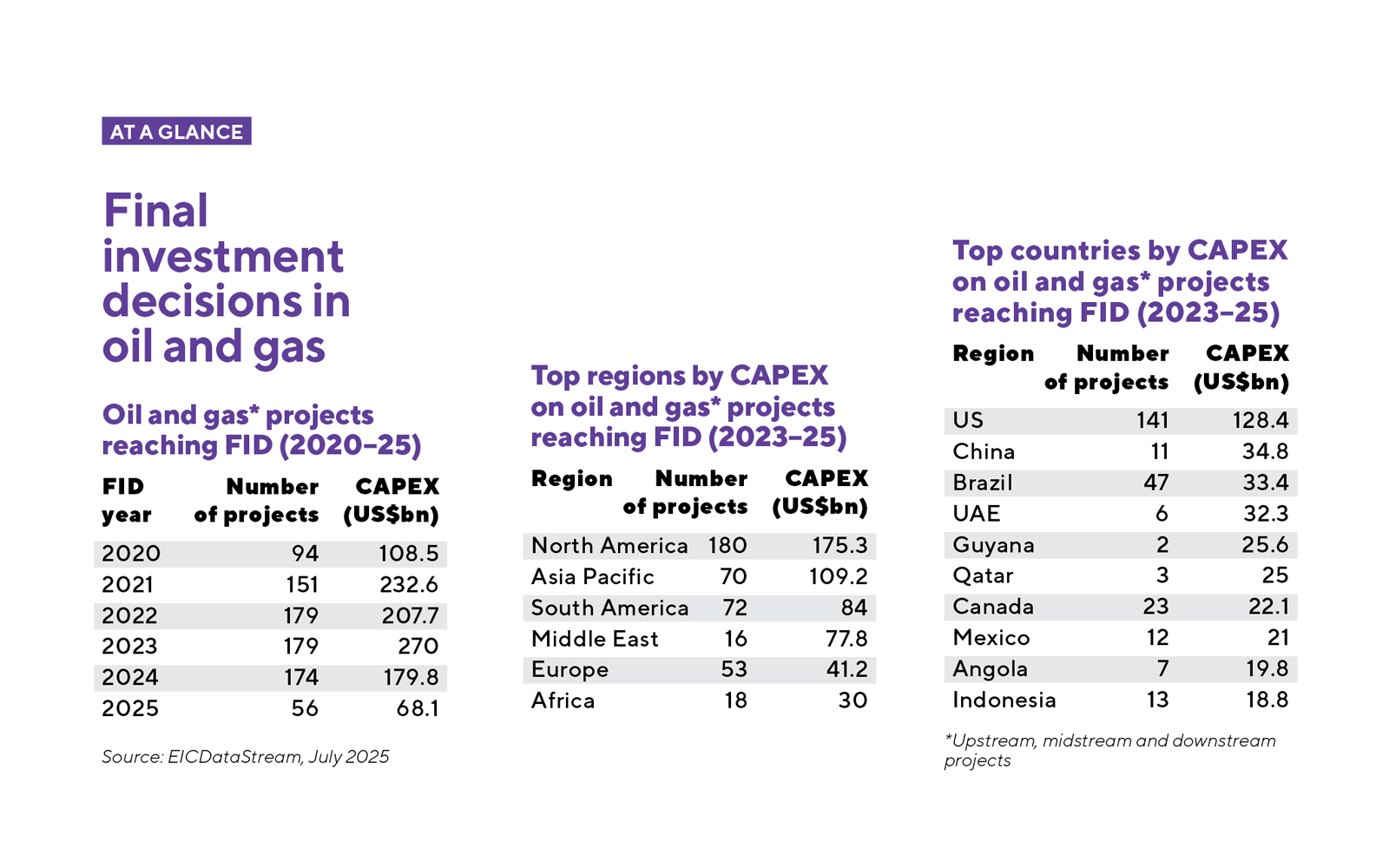

Since 2023, 180 oil and gas projects across the upstream, midstream and downstream sectors have reached final investment decision (FID) in North America, totalling US$175bn in investments. Of these, 36 are already operational. The US alone accounts for 141 of these projects, representing 73% of the total CAPEX.

Regionally, the midstream segment stands out, accounting for most sanctioned projects. Growing global liquefied natural gas (LNG) demand, combined with pro-export energy policies introduced under Trump, has driven midstream investment along the Gulf Coast.

Canada is also seeing renewed upstream investment and progress in LNG export infrastructure, marked by the recent first-ever commercial LNG shipment to Asia from the newly operational LNG Canada project. Despite recent progress, both Canada and Mexico have faced challenges linked to tariff policies introduced under the Trump administration.

In Mexico, the growing LNG export sector is further constrained by pipeline infrastructure bottlenecks, largely due to its dependence on imported gas from the US.

The outlook remains positive, driven by LNG growth and rising oil output in the US Gulf of Mexico. Furthermore, it is notable that North America’s role as a stable energy supplier is solidifying amid shifting global supply chains.

In Mexico, the growing LNG export sector is further constrained by pipeline infrastructure bottlenecks

Offshore growth and LNG ambitions in South America

In South America, the oil and gas sector is experiencing increasing activity. Since 2023, 72 projects across the upstream, midstream and downstream segments have reached FID, representing a combined CAPEX of more than US$84bn. Most investment targets exploration and production projects, as the region’s large offshore reserves continue to drive demand for floating, production, storage and offloading (FPSO) units.

By 2030, 20 FPSOs are expected to come online, with key developments in Guyana’s Stabroek block, led by ExxonMobil, as well as Brazil – the region’s leader in project number and investment – and Suriname, following TotalEnergies’ recently sanctioned GranMorgu project. There are 13 FPSOs scheduled in Brazil alone, nine of which will be operated by Petrobras.

This momentum is reinforced by successful bid rounds in Brazil and Guyana, and ongoing exploratory activities in both countries as well as Suriname, supported by steadily rising oil and gas demand through to 2050.

North America is the most active region globally in terms of sanctioned oil and gas project development

In Argentina, vast Vaca Muerta gas reserves are driving the country’s efforts to become a leading LNG exporter, with key projects moving forward. As an example, Southern Energy’s US$670m LNG terminal, approved earlier this year, aims to export 1Bcf/d by 2028 via two floating LNG vessels in the San Matías Gulf. These capital-intensive projects account for a large share of the US$5bn in investments sanctioned since 2023.

While challenges such as political instability, underdeveloped infrastructure and supply bottlenecks persist, South America’s vast reserves and ongoing developments, especially in offshore and LNG, underpin a positive outlook, positioning it as a key player in global energy supply diversification.

Asia Pacific: Exploration and gas-to-power expansion

The Asia Pacific region has been one of the top three most active hubs for sanctioned oil and gas investments in recent years, with around 70 projects across the upstream, midstream and downstream segments accounting for more than US$109bn. Active mega upstream projects, including the Abadi and Kutei North Hub, are progressing steadily, with FID expected in the coming years. Additionally, exploration activity is projected to rise as operators prepare for new drilling campaigns, with several companies across Southeast Asia having already secured drillships.

Licensing rounds throughout 2025 and 2026 across Malaysia, Indonesia, Brunei, Thailand, Pakistan, India, Vietnam and Bangladesh are expected to spur further exploration, feeding into future field development projects. Rising gas demand is fuelling new midstream infrastructure projects, with countries including Vietnam and Indonesia aiming to convert power plants to gas-fired plants. Governments are ramping up incentives for the industry to accelerate this shift.

Other nations have also fast-tracked LNG-to-power targets, though many projects still face investment hurdles. While cost pressures remain a challenge, the region’s robust project pipeline and strong government backing suggest sustained growth ahead.

Are you ready to export? Email: mariana.messere@the-eic.com

Image credit | iStock

Follow us

Advertise

Free e-Newsletter