Bankability shifts across global energy investment projects

As countries turn inward, the flow of capital is shifting – and so is the bankability of major projects. Two years of EIC final investment decision data show where investment is going, which sectors are thriving and how finance is evolving.

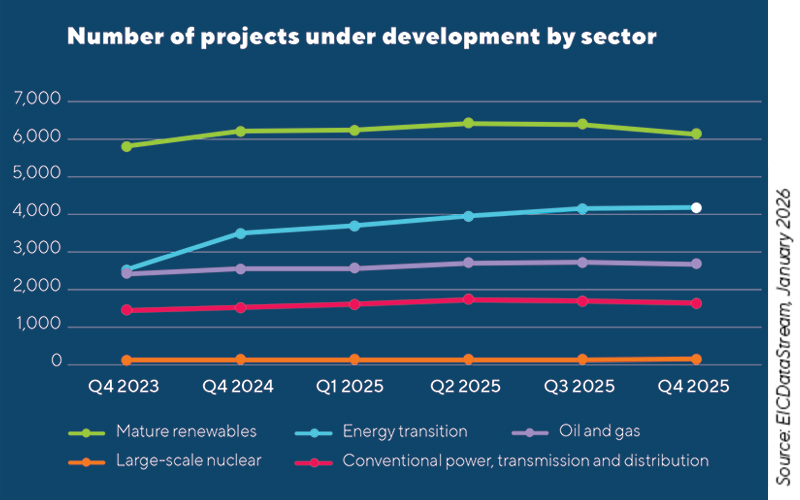

Demand, in the form of offtake or power agreements, is a significant factor in whether projects reach final investment decision (FID). Hydrocarbon demand shows no signs of slowing, with high-CAPEX upstream and midstream developments reaching FID. While some face delays – due, in part, to increasing costs – operators and developers continue to invest, knowing that demand will continue. However, operators will not invest without a fiscal regime and government support, as witnessed in the UK, where no projects reached FID.

Clean power demand is also rising. Investors understand onshore wind and solar well and some regions still offer government subsidies, making projects a ‘safe bet’; an increasing number are reaching FID. More offshore wind projects have also reached FID in the past two years. These require more capital outlay than onshore and are enabled by government subsidies, without which they would be less commercially viable.

A rising number of energy storage projects are reaching FID, too. As renewable power generation grows, battery energy storage systems – increasingly co-located with onshore renewable developments – are needed to stabilise grids and integrate variable renewable energy.

Despite high costs, the number of nuclear projects is growing as demand for clean baseload power rises. While small modular reactors will play a role, the sector is in its infancy and, in some instances, requires finalisation of regulatory policy before projects can proceed.

Demand for conventional power generation, specifically gas, is also growing – partially attributable to data centres, which require 24/7 baseload power. With this growth in power generation projects, grid investment is needed, and there has been an increase in the number of transmission and distribution projects reaching FID. This is long overdue and will be critical in ensuring that power can be distributed to demand centres, as well as providing grid resilience to support the green power generation transition.

Struggling sectors

It is easier to secure finance for sectors that involve mature proven technologies and clear demand than for energy transition sectors such as hydrogen, clean fuels and carbon capture. While more projects in the latter category have been announced and are reaching FID, it is not at the expected volume.

There is demand for clean fuels, and mandates have been set for sustainable aviation fuel (SAF), but projects are struggling to move forward. Large-scale projects have been paused or even cancelled (for example in the Netherlands) due to financial viability issues, rising costs (including feedstock prices) and investors wanting better financial returns. Clean hydrogen faces similar problems.

Operators will not invest without a fiscal regime and government support, as witnessed in the UK, where no projects reached FID

Several clean fuel projects have been cancelled due to increasing costs, policy and regulatory uncertainty (particularly in the US) and a lack of public funding, which lead to economic viability issues and operators shifting towards more commercially viable sectors. Projects that do reach FID all have long-term offtake agreements and are often close to where the fuel will be used.

Regional trends

South America’s upstream sector has seen continual investment, driven by large-scale, multi-billion-dollar floating production, storage and offloading unit projects in Brazil, Guyana and Suriname. However, financial difficulties have limited the number of midstream and downstream projects reaching FID. Risks are perceived as high, especially for large-scale export projects, which compete with lower-cost global markets such as China and the Middle East.

Large-scale CAPEX oil and gas projects are reaching FID in the Middle East – no surprise given hydrocarbons’ importance to the region’s national economies. There has also been more cleantech activity, particularly in solar; with some of the world’s highest solar irradiance levels, solar power generation here is efficient and effective. This activity has been enabled by government initiatives and policies such as Saudi Vision 2030, which includes clear renewable energy targets and financial incentives. The region’s low solar power tariffs also make it attractive to domestic and foreign investors. Hydrogen developments, however, are not proceeding – demand is not at expected levels, and projects such as those at Duqm in Oman are being cancelled.

Government support and policies are needed for many projects to reach FID. This is seen in Europe, which has the highest volume of hydrogen projects reaching FID thanks to strong EU funding (such as from the European Hydrogen Bank), policy certainty and energy operators’ vision for a continent-wide network. However, the sector is yet to see expected demand, and 2030 production targets are unlikely to be met. Offshore wind, meanwhile, has been supported by policies and financial frameworks such as the Contracts for Difference Mechanism, giving investors certainty that projects are commercially viable.

Policy certainty is critical for investor confidence – and policy change has been felt significantly in North America, particularly the US. The number of hydrogen and SAF projects reaching FID fell in 2025 due to policy and regulatory uncertainty, as well as the absence of long-term offtake agreements. Without guaranteed demand for their products, projects cannot secure investment. One US sector that is thriving thanks to global demand is liquefied natural gas (LNG) liquefaction, with six projects reaching FID in 2025. This sector also gained regulatory clarity after the permitting pause was lifted, giving developers and investors the confidence to invest.

Other than China, the Asia Pacific region has seen little progress in the energy transition sectors. Many countries have yet to finalise regulations needed for projects to be developed, leading to low investment levels. However, oil and gas projects continue to reach FID: governments are supportive of the sector and FIDs have been reached for significant projects such as Hidayah and Kelidang in the past 12 months, with more expected.

It is easier to secure finance for sectors that involve mature proven technologies and clear demand

Africa has seen the lowest value of projects reach FID. While energy companies have invested in oil and gas projects, FID has been delayed; political and economic risk are often cited as issues for investors, making projects less financially viable. When it comes to renewables, existing power grids lack the capacity to integrate new sources, and a lack of policy and regulation is a further barrier.

Making it bankable

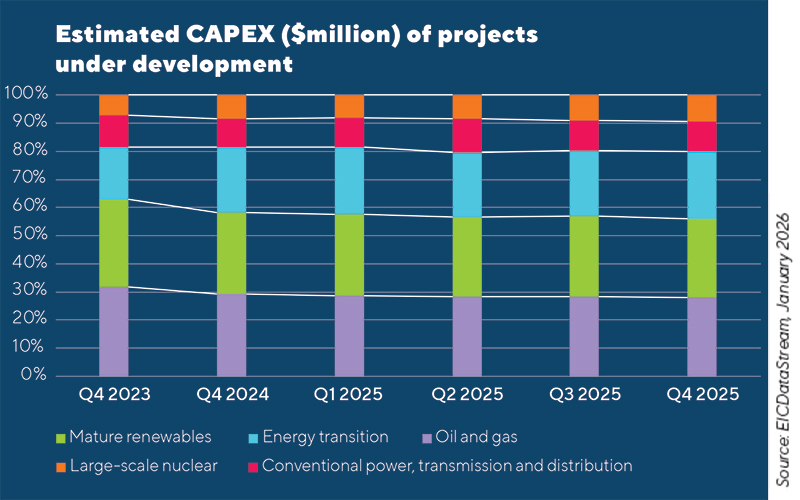

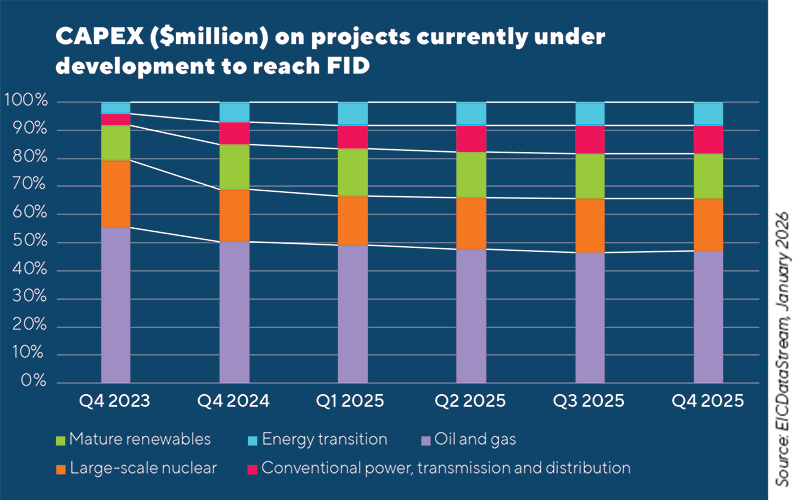

Capital flows most readily where demand is clear, technologies are proven and policy frameworks provide certainty. Hydrocarbons and conventional power continue to attract investment, while mature renewables, storage and grid infrastructure benefit from established financing models and government support.

Transition sectors such as hydrogen, clean fuels and carbon capture face slower progress, constrained by cost pressures, regulatory uncertainty and insufficient offtake. Ultimately, bankability hinges on aligned demand, supportive policy and fiscal stability – without which even strategically important projects struggle to advance.

Deep dive

What makes projects bankable?

By Mahmoud Habboush, EIC Bankable Energies Report Author

EIC data on the projects moving to final investment decision (FID) matches industry leaders’ experience: bankability improves with robust offtake agreements, commercially viable economics, controlled technology and delivery risk, and stable, predictable policy.

I spoke to 50 UK-based energy leaders and executives across developers, contractors, advisers, lenders, insurers and supply chain firms. The interviews – conducted for the Bankable Energies Report, to be released at the Bankable Energies Conference on 17 March 2026 – focused on what makes projects bankable, what stops them progressing to FID, and why capital goes to sectors where healthy demand, technology availability and policy stability align.

For many energy executives, revenue certainty is the starting point – specifically long-term power purchase agreements, Contracts for Difference and commodity-linked offtake agreements as mechanisms that allow lenders to model cashflows and make informed decisions on debt size. When these contracts have credible counterparties, projects move through investment committees with fewer assumptions and less pricing friction. If price, tenor or buyer strength are weak, projects stall – even when engineering looks robust.

For major national projects, interviewees said that government-backed revenue schemes are decisive enablers, citing regulated asset base-style models, cap-and-floor regimes and termination compensation as mechanisms that reduce construction and volume risk; carbon capture, transport and storage was a recurring example. Projects depend on both emitters and shared networks reaching operation on aligned timelines. Energy industry stakeholders argued that governments can bridge this coordination risk to make debt possible where private contracting cannot.

Policy stability and fiscal credibility are crucial, with interviewees tying bankability to durable policy direction, cross-party alignment and stable taxation; dozens of energy leaders have told us this across multiple EIC research projects, including our annual Survive & Thrive research initiative and the Net Zero Jeopardy reports.

Energy executives said that investors hesitate when fiscal rules are reset within short periods or permitting requirements change late in development. UK oil and gas was repeatedly cited as an example of projects being deterred through stifling taxation and approval criteria, despite demand; developers cannot forecast returns across a multi-year project and payback period. The same applies even in low-carbon sectors that rely on subsidy or price-support policy. If political risk rises, lenders price uncertainty into debt and developers freeze work.

Project delivery issues also affect bankability. Several participants described projects where the technical case was acceptable and the revenue model was improving, but the contracting model could not be agreed. For example, one developer tried to secure a full lump-sum turnkey contract for a complex energy transition build while scope and performance parameters were still being refined; tier-one contractors would not take on combined schedule, productivity and performance risk under that structure. The developer had to either add a high-cost contingency that weakened the business case, or pause procurement and make the risk allocation acceptable to the market.

Capital arrives where there is stable policy, bankable demand, established revenue models and deliverability

Skills availability is another issue, with UK infrastructure builds competing for welders, fitters, scaffolders, commissioning staff and project managers. If multiple projects launch in one region, the risk of wage escalation and workforce turnover rises. This ties in with supply chain bottlenecks in cables, transformers, foundry capacity, ports, vessels and specialist fabrication.

Finance and insurance executives focused on data quality, noting that projects make better progress when owners and managers provide solid technical data, credible performance evidence and clear scenario analysis.

The interviews also explained why transition projects progress slowly. Hydrogen and clean fuels struggle with weak offtake potential, uncertain pricing benchmarks, high CAPEX and policy dependence. Energy executives noted that projects reaching FID tend to secure long-tenor offtake and align location with end use to reduce logistics and demand risk. Several added that the absence of a revenue bridge for sectors such as sustainable aviation fuel leaves projects exposed to feedstock costs, return expectations and policy change.

Capital arrives where there is stable policy, bankable demand, established revenue models, deliverability, and other factors such as supply chain and infrastructure capacity and fiscal stability. If one element fails, projects face delays, restructuring or cancellation.

By Neil Golding, Director of Intelligence, EIC London

Image credit | iStock

Follow us

Advertise

Free e-Newsletter