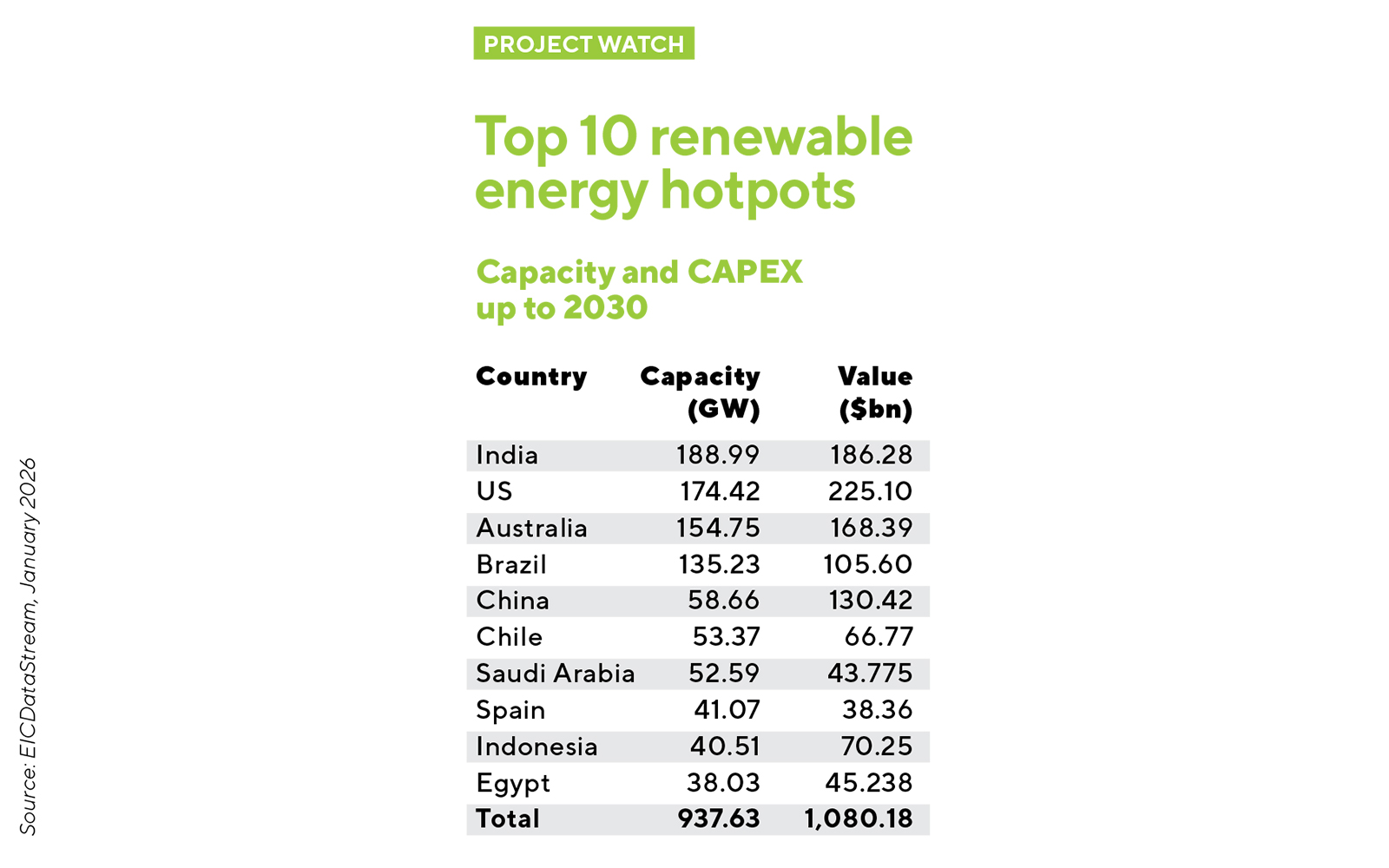

Renewables accelerate as energy security and supply chains reshape markets

Nabil Ahmed explains what is driving investment in renewable energy, which emerging markets are gaining momentum and where the largest supply chain opportunities are likely to emerge over the next few years.

What is driving investor interest in renewables right now?

Investor interest in renewable energy across the globe is being propelled by a powerful mix of economic, policy, technological and risk-related factors. Solar and onshore wind are now the cheapest forms of renewable electricity in most regions, supported by mature and well-established supply chains. This has significantly increased investor confidence in financing such projects.

Technology costs have fallen sharply over the past decade – solar PV generation costs alone have dropped 83% since 2010 – making renewables increasingly competitive with, and often cheaper than, fossil fuel alternatives. At the same time, geopolitical instability and volatile fossil fuel markets have also prompted many nations to prioritise energy independence. Investing in domestic renewable sources is a strategic way to secure a stable and reliable energy supply.

Which emerging markets are you watching most closely?

Across Europe, several markets are experiencing rapid growth despite not yet being fully mature. Germany, Spain and Denmark are benefiting from policy reforms, EU funding mechanisms and rising energy security needs.

Poland, in particular, has seen strong onshore wind and solar growth, alongside major offshore wind developments. It recently awarded contracts for 3.5GW of offshore capacity in its first offshore wind tender.

Romania is another market to watch, having awarded more than 300MW of onshore wind capacity through its third Contracts for Difference (CfD) auction. Latvia is also emerging as a promising market, with a growing focus on large-scale onshore wind and solar supported by EU funding and investment from international developers.

Will the 2030 industry targets for offshore wind be met?

It is widely projected that many countries, including the UK and US, will fall short of their national 2030 offshore wind targets. Some consider the targets too ambitious, but global capacity is expected to nearly triple by 2030 – a sign of huge growth.

Several challenges are expected to prevent countries from meeting their ambitious goals. The primary issue is supply chain bottlenecks: a global undersupply of specialised installation vessels, overloaded fabrication yards and limited port infrastructure are causing project delays and increasing costs. Rising costs and funding issues due to inflation and increased capital costs have led to project cancellations and made investment more challenging. Permitting and regulatory delays from lengthy planning and consenting processes, which can take up to a decade, are also a major barrier to rapid deployment. These constraints all add to the difficulty of developing the sector.

Denmark, Germany, Latvia, Poland and Spain are growing quickly due to policy reforms, EU funding mechanisms and rising energy security needs.

What needs to happen for the industry to get close to these targets?

The 2030 targets were deliberately set at ambitious levels to stimulate market growth and have largely succeeded in driving momentum. However, urgent policy support and investment in infrastructure are needed to bridge the gap and stay on track with the broader global goal of tripling renewable energy capacity by 2030.

To achieve offshore wind targets, the industry needs increased government auction budgets (such as the CfD scheme), stronger port infrastructure, expanded port capacity, a skilled workforce and streamlined permitting. Furthermore, long-term supply chain investment with clear future pipeline visibility is essential, shifting focus from pure competition to scale and reliable delivery – especially for floating wind technologies – all of which would massively assist in achieving these ambitious targets.

Where are the biggest supply chain opportunities for EIC members in the next two to three years?

The biggest opportunities will be found where investment, deployment and local content demands are strongest. With major offshore wind projects underway, a broad chain of goods and services is scaling up, including turbine blades, specialised installation and maintenance vessels, port infrastructure and logistics, and floating wind components. This will also include shipbuilding and service fleets, reinforcing the demand for maritime industry expansion. If regions can develop local production hubs, there will be much more demand for blades, electrical systems and service infrastructure.

While solar panels and wind turbines are popular, most supply chain value comes from the balance of systems – the components around core generation technology such as mounting systems, inverters, cables and transformers for solar and wind farms. Foundations and electrical balance infrastructure can constitute around 60–70% of total project spending and are easier for new suppliers to enter, compared to panel or turbine manufacturing.

Battery energy storage systems, both large-scale and distributed, are accelerating as grids integrate more renewables, offering a solution to grid constraints. An increasing amount of battery capacity is being added and co-located with other sectors such as onshore wind and solar. Energy storage supply chains are still scaling relatively quickly compared with solar and wind, highlighting the significant opportunity in this sector.

Want to know more about the current state of the renewables market?

Contact: nabil.ahmed@the-eic.com

Image credit | iStock

Follow us

Advertise

Free e-Newsletter