Why conventional power is back

Aisyah Sarjuni discusses the resurgence of gas, coal and nuclear, investor trends and opportunities for industry players as geopolitical tensions and supply chain challenges reshape the conventional power sector.

How are geopolitics and supply chain pressures reshaping the industry?

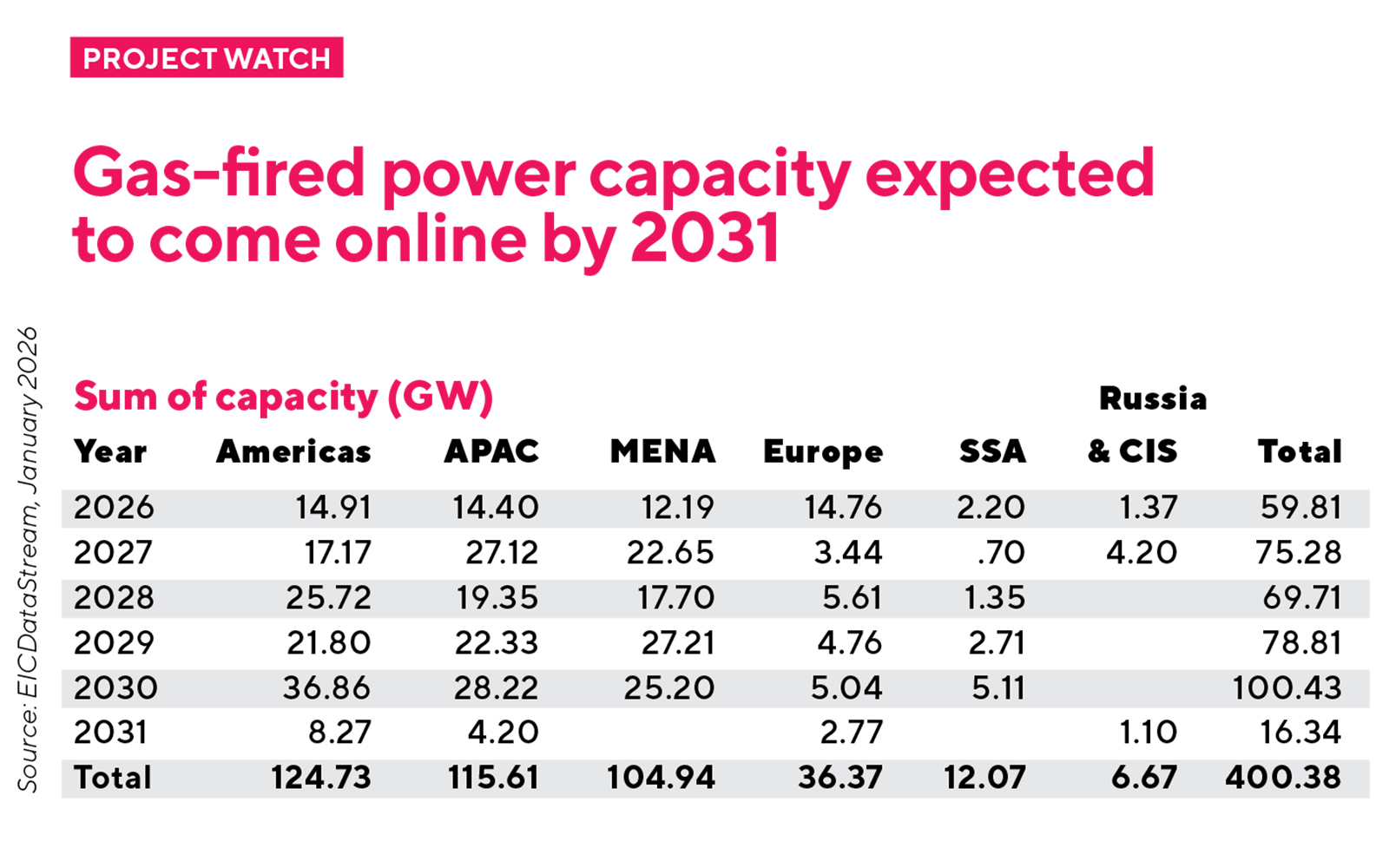

Global energy players are pivoting back to conventional power as a reliable and cost-effective energy source. Significant trends include the resurgence of nuclear power, the delayed decommissioning of coal power plants and the significant shift towards gas power plants. Asia Pacific and North America are leading in conventional power investment (excluding nuclear), with projected CAPEX of US$416bn and US$166bn respectively.

The boom in the gas and liquefied natural gas (LNG) trade has created both opportunities and risks. Today, the gas supply chain is evolving beyond energy security to become an important diplomatic currency. The US recently signed long-term LNG deals with multiple developing countries, including Malaysia and Greece, making fuel pricing sensitive to shifts in US trade policy and dynamics.

Besides the complex gas and LNG trade, the surge in gas turbine demand has led to supply chain bottlenecks. With total turbine orders of 54.9GW capacity across GE Vernova, Siemens Energy and Mitsubishi, the Big Three turbine suppliers have announced plans to intensify manufacturing capacity over the next few years. Siemens Energy is currently the leading supplier, with around 52 active contracts globally for gas-fired projects.

What’s the market’s biggest misconception about power generation?

That choosing an energy source is a trade-off between green or conventional. Between 2020 and 2024, renewables grew not just as part of energy transition but also as an economic recovery tool. However, in 2025, cost and energy security remained crucial.

Renewable growth continues, supported by the battery energy storage system market; however, supply chain hurdles, power density, grid constraints and intermittency remain significant challenges. This highlights the importance of balancing green ambitions with operational reality, especially in the face of energy security concerns and booming datacentre developments. Europe offers a clear example: despite strong green mandates, conventional power projects grew by 31% in 2024–2025 to meet rising baseload demand.

What is driving investor interest right now?

Interest in alternative fuels, such as hydrogen and ammonia, has slightly dipped due to lower projected returns and demands, but they remain an important decarbonisation tool in the conventional power sector. To comply with decarbonisation goals, there has been interest in multi-fuel turbines – especially hydrogen-ready gas turbines. The US alone has 23.6GW of planned hydrogen-ready gas-fired power plants by 2030.

In addition, the expansion of carbon capture initiatives is increasingly supporting the continued development of gas-fired projects, allowing governments to retain firm capacity while cutting emissions. The integration of carbon capture technologies is a growing trend in the power sector. Saudi Arabia is investing more than US$17bn into the integration of carbon capture and storage (CCS) technology for 17GW of its overall gas power pipeline. Meanwhile, the UK government’s 2026 National Policy Statement recently highlighted that new gas plants must be built ‘decarbonisation ready’, with carbon capture utilisation and storage technology or hydrogen-ready turbines.

What project pipeline trends should EIC members prepare for?

The focus is on getting enough baseload power to meet datacentre, industrial and domestic demand. The power dilemma is driving electricity prices upwards. More gas peaker plants are being developed to address power shortages – prominently in Europe, as well as in countries such as the US, Indonesia and Vietnam. While the cost of peaker plants can be greater than renewable power, they prevent significant losses from load shedding, strengthening grid stability. As grid congestion reaches an all-time high, new baseload builds may take longer to begin operations.

Grid congestion is delaying new baseload projects, highlighting opportunities for upgrades and modifications of existing nuclear, coal and gas plants

Grid congestion is delaying new baseload projects, highlighting opportunities for upgrades and modifications of existing nuclear, coal and gas plants. Iraq, for example, is converting thermal plants to gas turbines while boosting capacity.

Cross-border interconnectors such as the GCC Grid Interconnector, linking Oman, Kuwait and Southern Iraq, are also critical to enhance grid stability.

Where are the biggest supply chain opportunities for EIC members in the next two to three years?

Facing grid constraints and gas turbine production bottlenecks, the market is expected to shift to asset optimisation. There is likely to be strong demand for upgrades to ageing plants, as well as AI-driven predictive maintenance services.

CCS technologies will be increasingly important as decarbonisation targets remain a priority. However, the expanding power market will struggle without proper grid infrastructure. Energy players should observe the transmission and distribution sector as there is a critical global need for modernised grid infrastructure to enhance connectivity and capacity. Some of its major supply chains include interconnectivity cables, high-voltage transformers and high-voltage direct current converter stations.

Want to know more about the current state of the conventional power market? Contact: aisyah.sarjuni@the-eic.com

Q&A with Aisyah Sarjuni, Energy Analyst, EIC Kuala Lumpur

Image credit | iStock

Follow us

Advertise

Free e-Newsletter