Nuclear's next decade: Markets, myths and opportunities

Jack Boggis examines where nuclear investment is accelerating, which emerging markets are gaining momentum and how the industry is addressing long-standing safety misconceptions as small modular reactors and rising energy demand reshape nuclear’s global role.

Which global markets look set to lead nuclear investment through 2030?

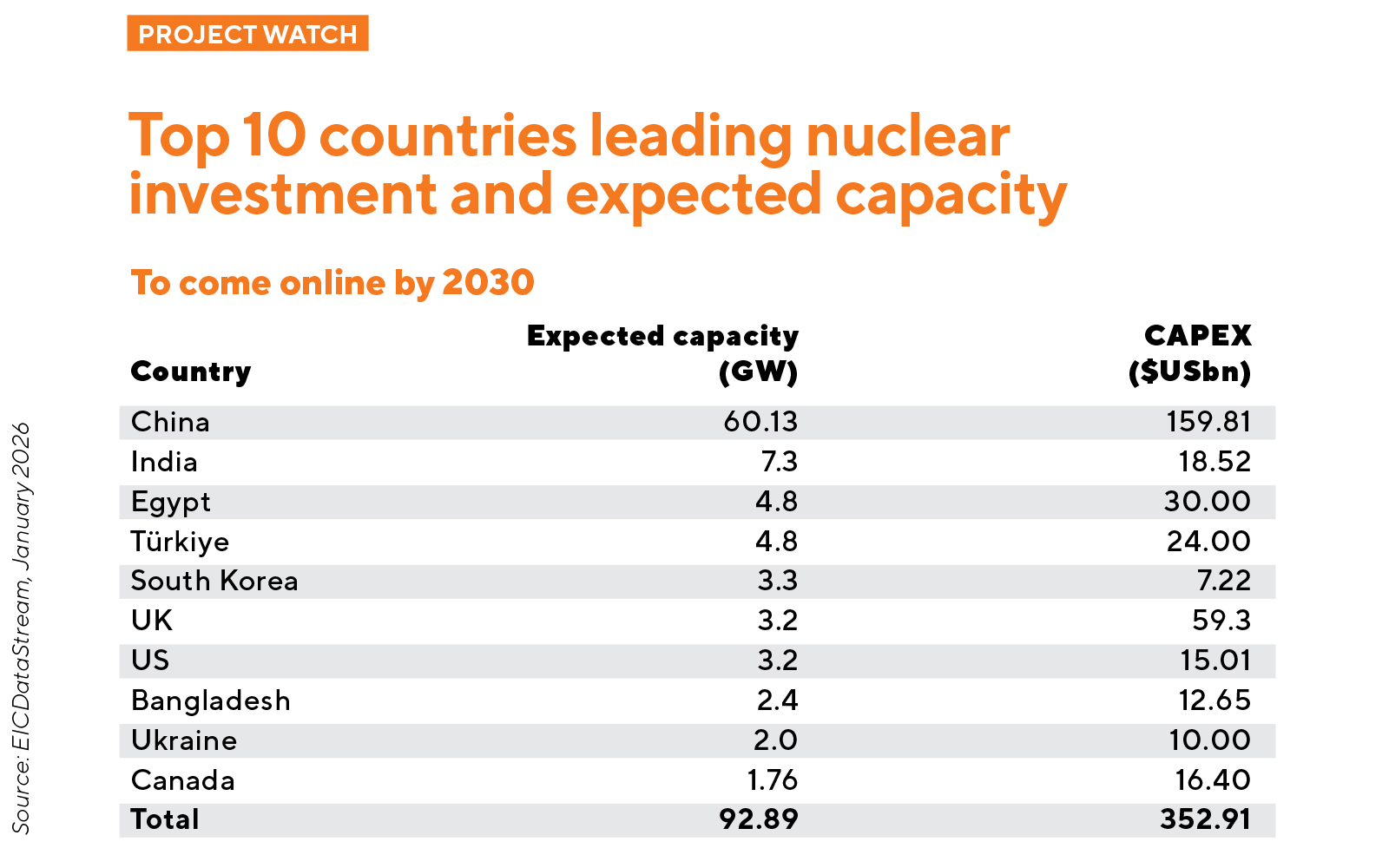

Global nuclear investment is expected to reach US$436bn by 2030. China is in the lead, with US$160bn in CAPEX spanning 60GW across 26 projects. The UK follows, with US$58bn focused on Hinkley Point C (3.2GW), while Egypt is set to commission its first nuclear plant with four 1.2GW reactors, representing US$30bn in total investment. The US and Canada are expected to ramp up investment beyond 2030, with the US aiming to quadruple capacity by 2050. The UK is also planning more investment through partnerships such as the UK-US Atlantic Partnership for Advanced Nuclear Energy, which announced four new small modular reactor (SMR)/advanced modular reactor (AMR) projects in 2025.

Which emerging markets are you watching most closely?

Europe is looking to become a major SMR market in the coming years, with Norway emerging as an important SMR developer to support the decarbonisation of its heavy industries, as well as remote areas where existing energy infrastructure struggles to reach. The country’s leading developer Norsk Kjernekraft signed a three-year cooperation agreement with Aecon in November 2025 to explore development of SMRs, focusing on GE Vernova Hitachi’s BWRX-300 reactor. The BWRX-300 is also being explored in Poland and Estonia, with the former choosing Włocławek as the first location in which to deploy it.

Czechia and the UK are also committed to advancing SMRs, focusing on the Rolls-Royce 470MW, which aims to position the two nations as leaders in the advanced nuclear sector. Czechia is planning 3GW of Rolls-Royce SMR capacity, with Temelín chosen as the first site. Czechian electricity distribution company ČEZ has also acquired a 20% stake in Rolls-Royce’s SMR division.

Keep an eye on Hungary, too; agreements have been signed with Holtec and Rolls-Royce to explore deployments of each developer’s technology.

What project pipeline trends should EIC members prepare for?

Data centres and AI are driving unprecedented energy demand, expected to consume the equivalent of Japan’s total power consumption by 2030. Nuclear is emerging as the ideal power source for data centres, with reactors able to provide continuous,

low-carbon electricity. This will be crucial in achieving net zero ambitions, as data centre infrastructure is highly energy intensive.

Major technology companies are exploring the use of SMRs to meet this demand, and several have signed power purchase agreements (PPAs) with SMR developers. Google, for example, will use 500MW of SMR capacity from Kairos Power to power its US data centres. It is likely that further SMR projects will be developed to support data centres in the future, and PPAs are an important way to support financing these projects, which are still in their infancy. Members should look out for more of these projects, especially between major technology companies and SMR developers.

Fusion energy is also being looked at as a power source for data centres, as shown by the largest fusion-related PPA to date: in July 2025, Commonwealth Fusion Systems signed a landmark agreement with Google, under which Google will procure 200MW of electricity from its ARC fusion project.

What is the market’s biggest misconception about nuclear?

Nuclear is still perceived as an unsafe form of energy production – when it is mentioned, people first think about its historical application in warfare, or nuclear power plant disasters, rather than how it has reshaped the way we generate electricity. Power plants have exceptional safety systems in place to suppress the fission process and prevent runaway chain reactions, and nuclear energy is one of the most heavily regulated types of energy in the world. Nuclear power is also getting safer as innovative technologies are introduced: SMRs and AMRs are gaining traction due to their smaller footprint and cheaper construction, but they are also deemed safer thanks to their simpler designs, which have more passive safety systems.

Nuclear energy faces a resurgence as countries aim to triple global capacity by 2050 due to its low-carbon nature and potential to help reach net zero

Nuclear energy faces a resurgence as countries aim to triple global capacity by 2050 due to its low-carbon nature and potential to help reach net zero goals. However, safety concerns are unlikely to go away any time soon.

Where are the biggest supply chain opportunities for EIC members in the next two to three years?

The SMR market is a big opportunity, but is still in the early stages of its journey towards becoming a major sector; this is likely to materialise from the mid-2030s onwards. The supply chain, however, would benefit from supporting the design and manufacturing of SMR components now. This will accelerate deployment once sites are ready to install the reactors, given that they are expected to be factory-built and then assembled on site.

Various existing nuclear reactors could see their lifespans extended, presenting opportunities such as component replacement, material testing and inspection, and assistance in complying with updated safety legislation. Some reactors, such as the Duane Arnold plant in Iowa, US, are even being restarted. This promotes whole-plant refurbishment, recertification of safety-critical systems and the provision of workforce retraining to ensure they are licensed and qualified to operate the reactors.

Want to know more about the current state of the nuclear market? Contact: jack.boggis@the-eic.com

Q&A with Jack Boggis, Energy Analyst, EIC London

Image credit | IKON

Follow us

Advertise

Free e-Newsletter