All eyes on LNG: key to tackling energy security and climate goals

Amid ongoing climate goals and heightened energy security considerations, global investments in the oil and gas sector have notably shifted their focus towards liquefied natural gas projects, says Fernando Vieira at EIC.

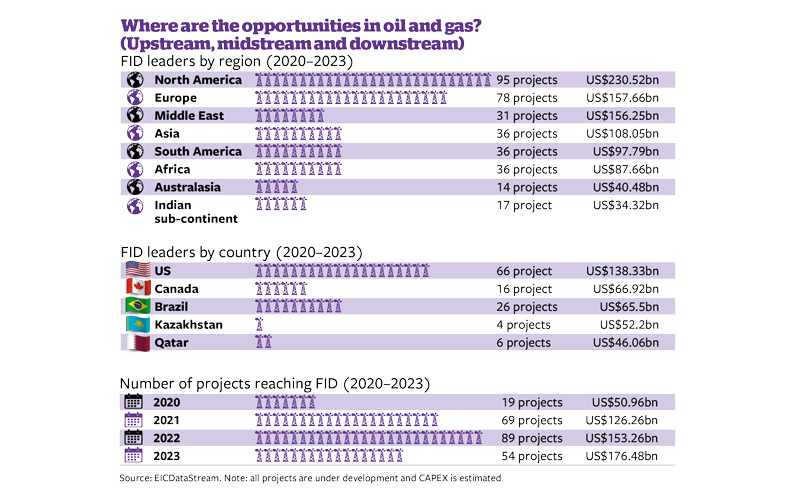

During the last six years, data collected by EICDataStream has revealed a significant trend towards higher investments in liquefied natural gas (LNG) production, liquefaction and regasification projects.

LNG: a catalyst for the energy transition

Investments in LNG, a transitional and less polluting fuel, have risen to prominence, playing a central role in the medium-term decarbonisation strategies of both Europe and the US. Moreover, these investments effectively tackle pressing energy security issues – particularly amid geopolitical tensions and economic uncertainties, as underscored by the ongoing Russia-Ukraine conflict.

In the first half of 2023, data from the US Energy Information Administration indicated that the US, Australia and Qatar secured the top three positions in LNG exports, with daily volumes of 11.6bn, 10.6bn and 10.4bn cubic feet respectively. Since 2021, these countries have consistently alternated among the leading positions in LNG production, liquefaction and export. Notably, Europe, Japan, and China were major destinations for regasification in 2022.

There is growing interest in floating storage regasification units (FSRU) and floating liquefied natural gas (FLNG) terminals, as opposed to conventional onshore terminals. However, it will be challenging to balance FLNG mobility, access to remote offshore gas fields, and the accelerated monetisation of resources against issues of scalability, output and higher initial investments. In response, there is a trend towards developing small-scale offshore liquefaction projects to reduce costs while preserving mobility.

North America: Gulf Coast is key strategic hub for meeting global LNG demand

Approved liquefaction projects are abundant in North America, particularly in the Gulf of Mexico. In the US, there are 16 onshore projects listed on EICDataStream, all anticipating a final investment decision (FID) within the next two years. Notably, terminals such as Driftwood and Plaquemines LNG Export in Louisiana are gearing up to initiate multiple liquefaction trains between 2024 and 2028.

Mexico and Canada are emerging as potential strategic suppliers in the LNG market. The Fast LNG project in Mexico is expected to begin commercial operations with its first train in January 2024. Following a successful FID in February 2023, the second phase of the project is set to add two new trains in 2025.

In Canada, British Columbia is a budding hub for LNG and FLNG projects, with numerous initiatives set to commence operations from 2025 to 2028. Particularly noteworthy is the establishment of a fully electrified small-scale LNG facility in Port Edward. This project, which secured its FID in June 2023, stands out as one of the most promising ventures in Canada.

The Middle East and Africa: continued influence and prospective projects

The Middle East, with Qatar at the forefront, and Africa, led by Nigeria, present enticing prospects in terms of projected CAPEX, expansion of liquefaction capacity, and ongoing construction projects.

Qatar Energy, operating 14 liquefaction trains at the Ras Laffan Terminal, made two FIDs for the expansion of the LNG Export terminal in February 2021 and May 2023. These expansions, totalling a US$32bn investment, are scheduled to start operations in 2027. Meanwhile, Nigeria is gearing up to expand the Bonny Island LNG Export Terminal, having secured an FID in 2019 to incorporate a new train at a cost of US$4.5bn; commercial operations are slated to begin in 2027. Another noteworthy project is the Yoho FLNG Vessel, expected to receive an FID in late 2023 or early 2024.

Europe and Asia: regasification is key to energy supply

During the past three years, Europe has become highly attractive for LNG imports, considering new regasification capacity and CAPEX. Major European importers such as Spain, France, the Netherlands and Belgium have emerged due to their operational assets. Countries such as Germany, Italy, and Poland are actively investing in LNG imports to decrease their reliance on Russian natural gas.

Since the Russia-Ukraine conflict broke out, the German government has encouraged investments in FSRUs and import terminals. Operational projects such as the Lubmin LNG terminal and Brunsbüttel Port, with increased regasification capacity, have begun operations, supplying power and heat to German homes and industries. Short-term opportunities in Germany include the second phase of the Brunsbüttel Port and a mid-scale LNG transshipment terminal in Rostock Port. Despite lacking an FID, both government-approved projects aim to start operations by 2026, starting construction in 2023.

The Ravenna FSRU in the Adriatic Sea stands out among projects in Italy. With a US$1bn investment and receiving an FID in September 2023, its operator, the Snam company, has contracts with BW LNG and Saipem for FSRU acquisition, installation and commissioning, expected to conclude by late 2024.

Japan, China and South Korea are at the forefront in Asia, with Taiwan and Vietnam also amassing substantial CAPEX and regasification capacity portfolios. Taiwan’s US$2bn Taoyuan LNG Project is in progress and is expected to start operations in 2025, featuring a regasification terminal with a capacity of 3m tonnes per annum (mtpa). Another notable venture is the Taichung Terminal, which has obtained all necessary government licences and is advancing steadily, boasting a regasification capacity of 4.1mtpa, even in the absence of an FID.

Five major LNG projects targeting FID in 2024/2025

Driftwood LNG Export Terminal (Phase 1)

- Value: US$14.5bn

- Country: US

- Operator: Storegga

- Start-up year: 2027

Lake Charles LNG Export Terminal

- Value: US$13.2bn

- Country: US

- Operator: Energy Transfer Partners LP

- Start-up year: 2030

Port Arthur LNG Export Terminal (Phase 2)

- Value: US$10bn

- Country: US

- Operator: Sempra Energy

- Start-up year: 2028

Elk-Antelope LNG Liquefaction Project (Papua LNG)

- Value: US$9bn

- Country: Papua New Guinea

- Operator: ExxonMobil

- Start-up year: 2026

Cameron LNG Liquefaction Plant Expansion (Train 4)

- Value: US$7.5bn

- Country: US

- Operator: Cameron LNG

- Start-up year: 2027

By Fernando Vieira, Energy Consultant, EIC.

Interested in exploring global oil and gas opportunities?

Inform your decision-making with the latest contracting activity and market research from EIC. To discuss your needs, email Muhammad Arif at muhdarifsyafiq@the-eic.com

Image credit | Shutterstock | iStock

Follow us

Advertise

Free e-Newsletter