Oil, gas and growth

Mariana Messere explores key trends in oil and gas investment, from liquefied natural gas growth and downstream modernisation to supply chain opportunities, outlining where capital is moving and how companies can plan through 2030.

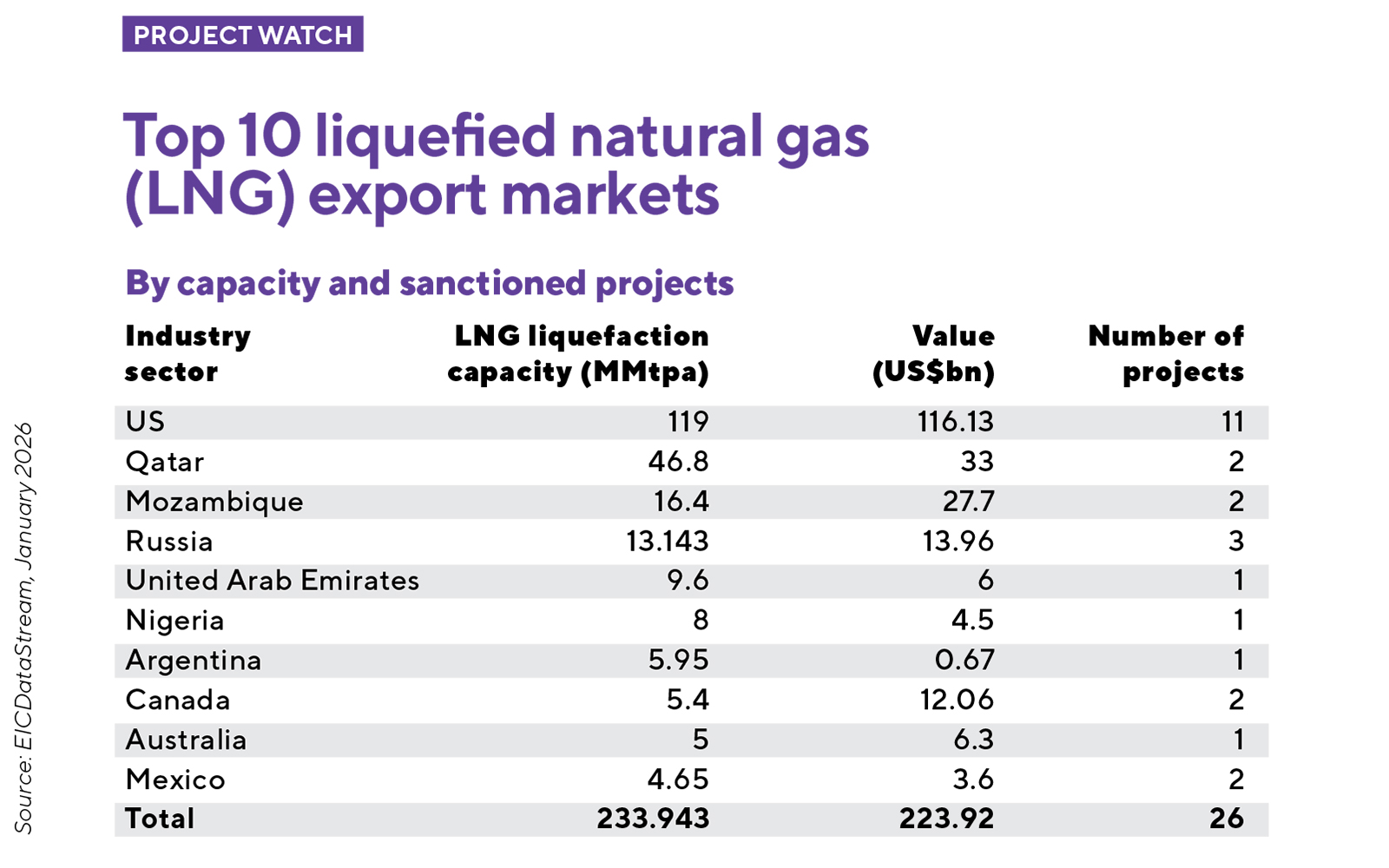

Will the investment levels seen in liquefied natural gas liquefaction in 2025 continue in the next two years?

Globally, the volume of new liquefied natural gas (LNG) liquefaction capacity scheduled to come online over the next few years is unprecedented, driven primarily by the US, Qatar and emerging second-tier producers. However, while investment peaked in 2025, this level is unlikely to be sustained in the coming years.

In the US – the world’s largest LNG exporter – the recent surge in final investment decisions (FIDs) reflects a backlog of relatively advanced projects that had previously been delayed by regulatory constraints. As a result, the near-term outlook is more construction-intensive. Even so, the US will remain the dominant LNG investment destination, supported by abundant shale gas resources, flexible commercial models and policy backing.

A sizeable LNG supply surplus is expected as new capacity ramps up. In the US alone, projects including Golden Pass, Corpus Christi Stage 3 and Plaquemines are due to come online from 2026, adding around 48mtpa of capacity. Beyond these, other projects that have also reached FID could contribute a further 120mtpa globally. If delivered on schedule, this supply surge is likely to put downward pressure on LNG prices, discouraging new project sanctions.

On the other hand, increased availability of flexible supply, including shorter-term contracts and destination-free cargoes, are likely to follow. There is also demand-side uncertainty: China reduced LNG imports in 2025, while Europe is expected to rely less on US LNG as renewables and energy-efficiency measures expand. As a result, greater reliance will fall on emerging Asian importers to absorb incremental supply, a trend that remains uncertain.

What downstream investment trends can we expect to see through to 2030?

EICDataStream is tracking more than 1,000 downstream projects worldwide that are expected to come online by 2030, representing more than US$1.2tn in CAPEX. Asia dominates by value, with more than US$291bn scheduled during the next five years. North America follows, with around US$213bn, but leads in project count, with 230 developments planned.

In the refining industry, activity is expected to be driven more by upgrades and expansions than by new builds. This reflects a structural shift in the sector, as global oil demand growth has slowed and the industry is increasingly concentrated in supplying products for petrochemicals.

However, petrochemical demand is progressively being met by natural gas liquids rather than traditional refinery outputs, while gasoline and diesel demand is expected to decline due to electric vehicle uptake and rising biofuel production and blending mandates.

In response, refiners – particularly in Europe and North America – are optimising product slates, improving efficiency and investing in petrochemical integration, emissions reduction and sustainable fuel production. By contrast, greenfield investments are concentrated in regions with industrial gaps, such as south-east Asia, Africa and the Middle East, where high CAPEX is directed towards new refineries and integrated petrochemical complexes.

Biofuels represent a major growth area, accounting for US$163bn of tracked CAPEX on EICDataStream to 2030. The US leads by value, with 86 projects representing US$27bn, supported by policy measures including proposed blending mandates and the extension of the 45Z Clean Fuel Production Credit, driving renewable diesel and sustainable aviation fuel projects.

Brazil, China and Indonesia are also significant markets. Brazil alone has 109 tracked projects, with sugarcane-based ethanol increasingly supplemented by corn-based production.

What project pipeline trends should EIC members prepare for?

Gas-related infrastructure is dominating oil and gas project pipelines. LNG, liquefaction, regasification, storage and associated pipeline projects remain central, driven by energy security concerns and the role of gas as a transition fuel. EICDataStream is tracking more than 135 proposed LNG liquefaction projects worldwide, with 103 expected to begin operations by 2030.

Beyond the US, capacity additions are led by Qatar, Canada and Mozambique, while suppliers in the Americas are gaining prominence, including in Argentina, Canada and Mexico. On the demand side, regasification terminals are expanding across Europe, Asia and South America.

Upstream activity is gaining momentum, particularly in high-value offshore developments across Brazil, Guyana, Suriname, Argentina and West Africa.Projects are increasingly being designed with energy-transition elements, including infrastructure for hydrogen and carbon capture, utilisation and storage, facilities capable of handling biofuels, and the electrification of platforms and assets.

The challenge is not to abandon oil and gas in favour of renewables alone, but to navigate a more complex and selective investment environment

What is the market’s biggest misconception about oil and gas right now?

A common misconception is that oil and gas investment is rapidly declining or becoming irrelevant due to the energy transition. Another is that the sector is unable or unwilling to adapt to climate realities. In reality, hydrocarbons will continue to play a central role in the global energy system, particularly given recent geopolitical tensions that have reinforced the importance of energy security.

At the same time, decarbonisation strategies and investment in sustainable processes are shaping industry decisions. Energy security today also means diversification of supply, which can align with transition goals and attract long-term investment in cleaner fuels, efficiency improvements, emissions-reduction technologies and gas infrastructure.

The challenge is not to abandon oil and gas in favour of renewables alone, but to navigate a more complex and selective investment environment.

Where are the biggest supply chain opportunities for EIC members in the next two to three years?

Across the gas and LNG value chains. Suppliers supporting liquefaction trains, compressors, storage tanks and export facilities are well positioned.

Upstream activity will also remain robust, with notable opportunities in South America. In the short term, Brazil and Guyana are set to lead offshore production growth. Brazil’s Petrobras is advanced in bringing a new generation of floating production storage and operation units (FPSOs) online, with seven new vessels projected by 2030. In Guyana, ExxonMobil Stabroek field development will see three FPSOs come online by 2030. Onshore, exploration of Argentina’s Vaca Muerta shale formation will support oil output growth in the coming years.

Refinery upgrades and modernisation present further opportunities, especially in digital solutions, automation, emissions monitoring and efficiency-driven retrofits. Midstream infrastructure – pipelines, terminals and storage – is another important growth area, led by the US, Canada and Indonesia.

Want to know more about the current state of the oil and gas market? Contact: mariana.messere@the-eic.com

Q&A with Mariana Messere, Energy Analyst, EIC rio de janeiro

Image credit | iStock

Follow us

Advertise

Free e-Newsletter