Unlock new oil and gas opportunities in Africa

Increasing exploration activities is a top priority for Africa’s resource-rich countries to alleviate energy poverty, ensure energy security and drive stability in global energy markets. As African oil and gas investment rebounds in 2022 and projects put on hold during 2020 and 2021 become part of the pipeline again, significant export opportunities exist for UK companies. EIC Analyst, George Blake, spotlights five emerging markets to watch

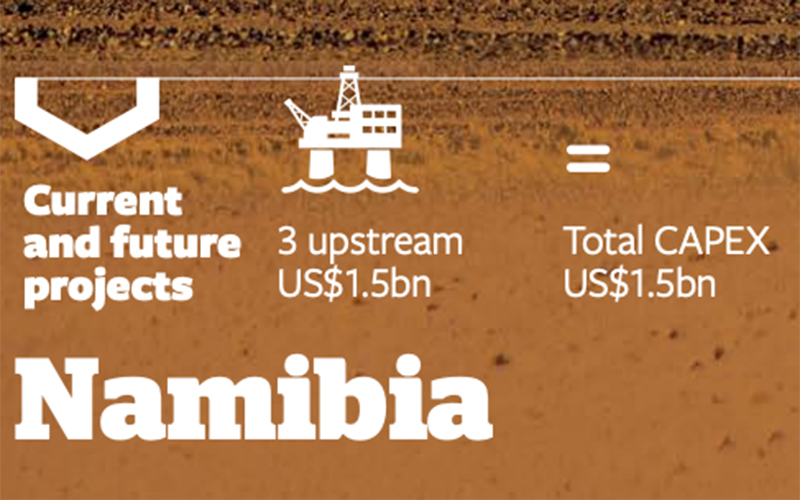

Namibia

Namibia’s natural resources are estimated at 11bn barrels (Bbbl) of oil and 2.2tn cubic feet (Tcf) of natural gas reserves, but the country has been characterised by unsuccessful oil and gas exploration projects, the only exception being the moderately-sized Kudu gas field discovered in 1974, which remains undeveloped.

Recently, the outlook has shifted. Following discoveries in neighbouring South Africa, Namibia’s offshore prospects have attracted many foreign companies. In February 2022, Shell announced that it had made a significant oil discovery in the Graff-1 exploration well in the Orange Basin at a depth of 3,000 metres. Two weeks later, TotalEnergies announced that its Venus-1X deepwater exploration well had also made a significant discovery of light oil with associated gas. These two projects could transform the Namibian economy, with reserves estimated at up to 2 Bbbl of oil equivalent (Bboe) and 3 Bboe, respectively.

Key players

Shell, TotalEnergies and BW Offshore are the key operators in the country, with Qatar Energy and Impact Oil and Gas Ltd also active in the Graff and Venus discoveries. The National Petroleum Corporation of Namibia has a 10% stake in Venus and Graff and a 5% stake in Kudu.

Future plans

There are reports that Shell may sanction at least one floating liquefied natural gas facility and a floating production storage and offloading unit (FPSO) for Graff; the size of Venus means it is likely to be produced via several FPSOs. The government is also hoping that Kudu can form part of a more holistic gas development in the Orange Basin and is encouraging Shell and TotalEnergy to fast-track their discoveries.

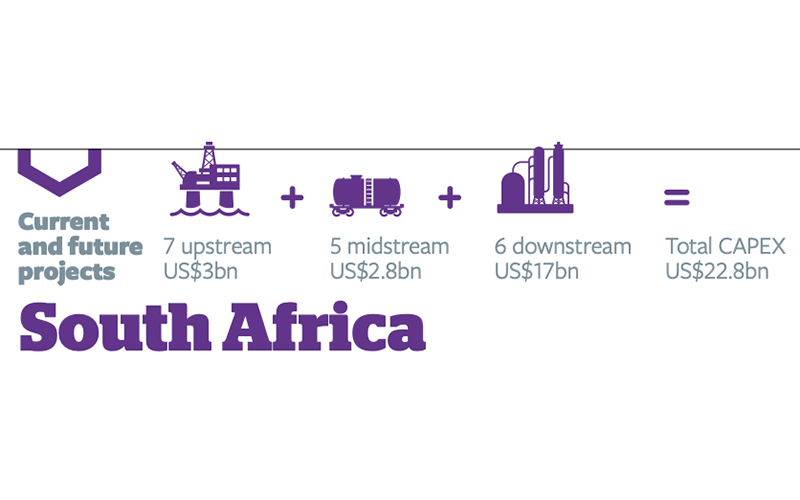

Although underexplored, South Africa has potential resources of 9 Bbbl of oil and approximately 60 Tcf of gas offshore. The recent Brulpadda and Luiperd discoveries (1.4 Bboe and 3 Tcf of gas collectively) suggest South Africa does have exploration potential, which should precipitate an influx of investment.

The South African government is putting oil and gas exploration at the forefront of numerous government development initiatives (the National Development Plan and the Integrated Resources Plan) and is actively working towards creating the legislative stability that investors want. The Upstream Petroleum Resources Development Bill also aims to encourage new entrants to the oil and gas sectors by facilitating invitation bid rounds (multiple bids for designated blocks).

Key players

Key players in South Africa include TotalEnergies, QatarEnergy, Saudi Aramco, Astron Energy, Canadian Natural Resources, Kinetiko Ebery, Badimo Gas, Renergen, Engen Petroelum Ltd, Umbono Capital and PetroSA (NOC).

Future plans

TotalEnergies hopes to use an early production system and existing infrastructure to fast-track Luiperd phase 1 exploitation. However, there are opportunities across all sectors to help South Africa build the infrastructure needed for large-scale gas development, particularly in a number of high-value downstream projects. Upstream opportunities should also grow, as exploration rights holders have expressed intentions to commence offshore drilling operations in the near future.

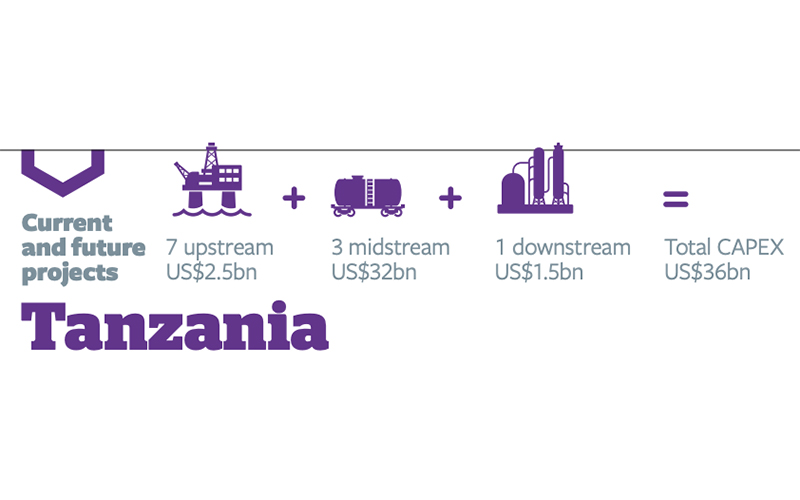

Tanzania has an estimated 57 Tcf of largely undeveloped gas reserves. Under former president John Magufuli, tax and contractual terms were hardened, production sharing agreements could be renegotiated where they were deemed ‘unconscionable,’ and projects were sidelined. Fortunately, new President Samia Suluhu Hassan is rapidly reversing this trend and shifting the country towards a more investor-friendly stance.

Key players

The Tanzania Petroleum Development Corporation (TPDC) is the custodian of exploration licences and has the right to participate in all gas projects across the entire value chain by holding at least a 20% shareholder stake. International companies that partner with TPDC include Aminex, Dosdal Resources, Equinor, ExxonMobil, Shell, MedcoEnergi, Pavilion Energy, Solo Oil and Shell.

Future plans

To meet its aim of a long-term economic growth rate of 7%, Tanzania is amending laws, working on receiving a credit rating and easing rules for doing business. The government is keen to provide the political, commercial and regulatory stability to fast-track existing projects and maximise their lifetime revenues. Hassan has revived talks on the Tanzania-Kenya gas pipeline and the US$30bn LNG Liquefaction Project, with reports suggesting that Shell has made substantial progress with the government in recent months.

Namibia

Kudu Gas Field

Value: US$800m

Start: 2026

Stage: Conceptual design

Status: Planning

Operator: BW Offshore

Venus Oil Discovery

Value: US$500m

Start: 2027

Stage: Exploration

Status: Drilling and appraisal

Operator: TotalEnergies

Graff Oil Field

Value: US$200m

Start: 2028

Stage: Exploration

Status: Drilling and appraisal

Operator: Shell

South Africa

Ibhubesi Gas Field

Value: US$1.4bn

Start: 2024

Stage: FEED

Status: Contract awarded

Operator: Umbono Capital

Brulpadda Gas, Condensate and Light Oil Discovery

Value: US$500m

Start: 2025

Stage: Conceptual design

Status: Planning

Operator: TotalEnergies

Luiperd Gas Condensate Discovery

Value: US$500m

Stage: Conceptual design

Status: Planning

Operator: TotalEnergies

South Africa Integrated Refinery and Petrochemical Plant

Value: US$10bn

Start: 2028

Stage: Feasibility

Status: Planning

Operator: Saudi Aramco

Tanzania

Tanzania LNG Liquefaction Plant

Value: US$30bn

Start: 2028

Stage: Pre-FEED

Status: Contract awarded

Operator: Shell

East Africa Crude Oil Pipeline

Value: US$3.5bn

Start: 2025

Stage: EPC

Status: Bids under evaluation

Operator: East Africa Crude Oil Pipeline

Block 1 Gas Discoveries

Value: US$500m

Start: 2028

Stage: Conceptual design

Status: Planning

Operator: Shell

Mauritania and Senegal

Mauritania and Senegal have transitioned from a frontier to an emerging opportunity. Projects include the ultra-deep, cross-border Greater Tortue-Ahmeyim (GTA) offshore field and the Sonamor Field development. In total, Mauritania and Senegal have 1.4 Bbbl of oil and 50 Tcf of gas reserves between them.

The Mauritanian government amended its Petroleum Code in 2014 to provide more incentives to attract foreign investment, and in 2017 it put access to electricity and developing domestic energy reserves at the heart of its Accelerated Growth and Shared Prosperity Strategy. Senegal has adopted a new Petroleum Code (2019) and Gas Code (2020) to provide a regulatory framework that can facilitate final investment decisions across all sectors. The government also established a committee, COS-Petrogaz, to steer and assist the management of natural energy resources. Senegal NOC Petrosen also launched its first offshore licencing round in 2020, covering 12 offshore blocks.

Key players

Kosmos Energy, BP, Woodside Petroleum, Cairn, Eni, CNPC and Far Limited are the active foreign players in current developments, while Shell, TotalEnergies, ExxonMobil and Atlas Oranto Group have exploration interests.

Both country’s NOCs, Petrosen and Mauritania’s Société Mauritanienne Des Hydrocarbures et de Patrimoine Minier, have an option to take a 10% stake in all contracts, and involvement of local companies is legislated for.

Future plans

The GTA FLNG project presents many offshore engineering equipment and service opportunities. The Mauritanian government also hopes to turn the port city of Nouadhibou into a regional gas hub and to expand storage capacity in Nouakchott by 150,000 metric tonnes. Following Senegal’s first offshore licencing round, there are opportunities to participate in field development and to provide supplies and logistical support.

Senegal/Mauritania

Greater Tortue-Ahmeyim FLNG

Value: US$2.2bn

Start: 2023

Stage: EPC

Status: Contract awarded

Operator: BP

Senegal

Sangomar Field Development

Value: US$4.6bn

Start: 2023

Stage: EPC

Status: Contract awarded

Operator: Rufisquue, Sangomar and Sangomar Deep Offshore JV (Woodside Petroleum, Cairn Energy, Far Limited, Petrosen)

Yakaar FLNG

Value: US$2.2bn

Start: 2026

Stage: EPC

Status: Contract awarded

Operator: Kosmos Energy

Mauritania

BirAllah Gas Hub

Value: US$2bn

Start: 2028

Stage: Planning

Status: Conceptual design

Operator: BP

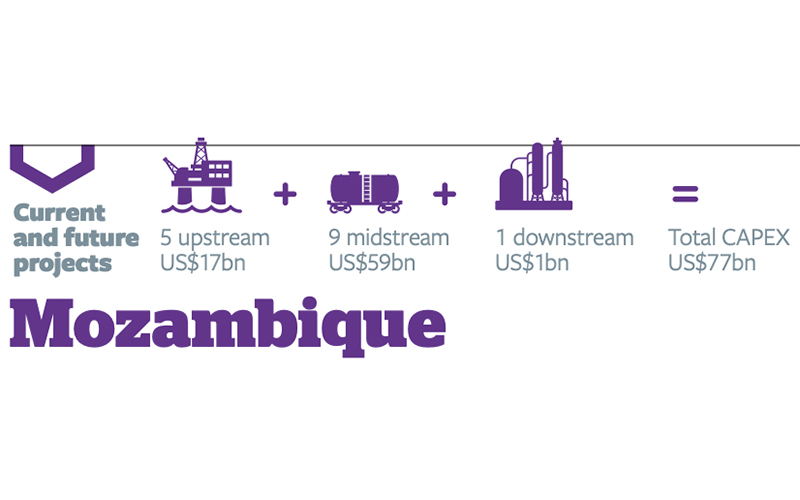

Mozambique has up to 100 Tcf of proven natural gas reserves, and current planned CAPEX stands at US$77bn – more than five times the size of Mozambique’s economy (US$14bn). Much of this investment is tied up in three LNG projects (two onshore and one offshore), but following Islamist terror attacks in 2021 within the Cabo Delgado region, both onshore projects were suspended. However, ongoing efforts to boost regional co-ordination and enhance security could precipitate a surge in activity, with projects expected to resume.

Key players

The LNG project operators are TotalEnergies, ExxonMobil and Eni, but around 20 foreign companies are involved, including KOGAS, Galp Energia, CNPC, Mitsui & Co, BPRL, PTTEP and ONGC Videsh. The NOC Empresa Nacional de Hidrocarbonetos de Mozambique holds a 10% or 15% stake in each.

Future plans

Once onshore projects resume, midstream opportunities will be numerous, especially as Eni plans a second FLNG to service its Coral South field. Growth is expected upstream, where Mozambique has attracted interest from some of the biggest majors in its latest licensing round (awards for all 16 blocks are due in November 2022).

Mozambique

Rovuma LNG Liquefaction Plant

Value: US$22bn

Start: 2028

Stage: EPC

Status: Project on hold

Operator: Mozambique Rovuma Venture (Eni, ExxonMobil, CNPC)

Mozambique LNG Project

Value: US$15bn

Start: 2025

Stage: EPC

Status: Project on hold

Operator: Mozambique LNG (Bharat Petroleum Corporation [BPCL], Mitsui & Co, PTT Exploration and Production [PTTEP], ENH [Empresa Nacional de Hidrocarbonetos de Mozambique], VideoCon Petroleum Ltd, TotalEnergies)

Area 1 – Golfinho-Atum Development

Value: US$4bn

Start: 2024

Stage: EPC

Status: Project on hold

Operator: TotalEnergies

Thinking of doing business in Africa? The EIC can help. Our team in Dubai is on hand to help you plan your path to overseas success. For more information and support please contact ryan.mcpherson@the-eic.com.

The EIC lists current projects in Africa and contact details on EICDataStream. Further details can be found at: www.the-eic.com/EICDataStream/AboutEICDataStream

By George Blake, Energy Analyst, EIC

Image credit | Shutterstock | Alamy

Follow us

Advertise

Free e-Newsletter