Venezuela's upstream potential

Following political shifts in early 2026, Venezuela’s vast oil and gas reserves are drawing renewed international interest. Regulatory reforms and foreign investments aim to revitalise the country’s struggling infrastructure and unlock its offshore gas potential.

The removal of Nicolás Maduro from Venezuela’s presidential chair in January 2026 has quickly brought the South American country back to the centre of international oil and gas discussions. The country holds a massive exploration and production potential: approximately 303bn barrels in proven oil reserves (17% of the global total) and total proven gas reserves of 200-300tn cubic feet.

Despite this, Venezuela is yet to see concrete returns from its resource base. Years of disinvestment and international sanctions have left the country’s oil and gas infrastructure in a critically deteriorated state, with weakened refining capacity and several deactivated upgrade units. The challenge facing the sector is therefore not only one of production, but also of processing, whether that means exporting crude overseas or modernising local infrastructure. On that front, US President Donald Trump has already declared his intention to bring Venezuelan oil to the US for refining and re-exportation.

Regulatory reforms attract foreign investors

Government reforms under Acting President Delcy Rodríguez are aiming to facilitate international players’ entrance (or re-entrance, in some cases) into the Venezuelan oil and gas business. The reform of the Organic Law on Hydrocarbons, announced in late January 2026, introduces fiscal flexibility measures that aim to provide greater assurance to foreign investors. These changes mitigate the risks for foreign companies and serve as an invitation to tap into the country’s vast natural resources, as the US simultaneously advances efforts to ease its sanctions on the country.

As this landscape consolidates, several major international operators are closely monitoring Venezuela’s movements and are likely candidates to return or pursue new business opportunities. Among the most prominent are American majors Chevron, ExxonMobil and ConocoPhillips, alongside European heavyweights Shell, Eni, Repsol and bp. China’s Sinopec, Chinese National Petroleum Corp and China Concord Resources Corp are also understood to be watching closely.

On the services side, Halliburton and SLB have already established footholds through involvement in several ongoing and planned projects, signalling broader industry confidence in the market’s trajectory.

Key joint ventures and operator movementss

Several concrete commercial moves have already emerged in 2026. Repsol has announced plans to increase its Venezuelan production by 50% in a year and triple output over the following three years through higher gas production, renewed oil infrastructure and the resumption of the Carabobo development via the PetroCarabobo joint venture (JV).

Chevron and Petróleos de Venezuela, S.A. (PDVSA) have agreed on an asset swap in which Chevron will divest its 25.5% stake in the Petroindependiente JV to PDVSA, which will assume control of the Loran and Macuira offshore gas discoveries. In return, Chevron will raise its stake in the Petroindependencia JV to 49% and gain rights to develop Ayacucho 8 through the Petropiar JV.

Eni and Repsol have shared plans to advance extraction from the Perla gas field by increasing production from the Cardon IV block from 580 to 645MMfc/d, alongside additional drilling and infrastructure upgrades. Eni and PDVSA have also agreed to relaunch the Junin 5 heavy oil project in the Orinoco belt.

Through JVs with other global players such as Indian Oil, Maurel & Prom and ONGC Videsh, PVDSA is advancing operations across Venezuela’s major resource plays, including heavy oil, light oil and offshore gas.

Unlocking offshore gas

Heavy oil and gas projects are the Venezuelan upstream industry’s two main levers. Looking at the location of these reserves, and at major projects such as Cardon IV, Macuira and Loran, around 40% of the country’s gas potential sits in its offshore acreage.

These projects are particularly vulnerable to geopolitical risks, given their heavy dependence on cross-border cooperation, liquefied natural gas export routes and the availability of third-party infrastructure. That combination of factors heightens exposure to political and commercial uncertainty and held back the pace of investment and development in the offshore gas sector throughout the Maduro years.

The challenge is now to develop a market that can capitalise on this offshore gas potential. As regulatory reforms and commercial activity gather pace, tangible effects are expected to emerge over the coming months – with Venezuela firmly in the spotlight of the international oil and gas industry.

Global Trends

Where the capital is flowing

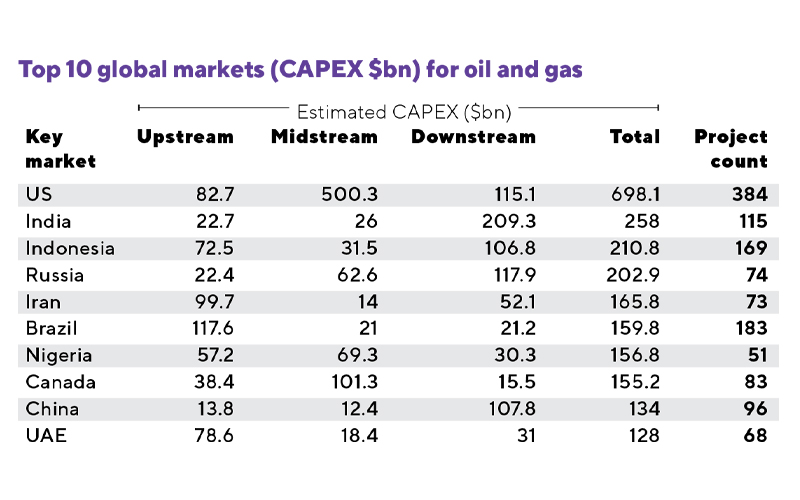

EICDataStream data reveals the regional trends and investment priorities that are shaping the global oil and gas landscape

EICDataStream is tracking 2,712 projects with an estimated CAPEX of US$4.12tn, led by Asia Pacific (APAC), North America and the Middle East. The oil and gas market in APAC is predominantly downstream-led. This sector accounts for approximately 50% of the region’s total CAPEX (US$635.6bn), driven mainly by the refining and petrochemical industries in India, China and Indonesia. The region is also advancing e-fuels such as e-methanol and e-sustainable aviation fuel. Upstream follows with US$285.9bn, supported by active exploration and licensing rounds across Malaysia, Indonesia, Brunei, Vietnam and India. Strategic moves such as Eni’s collaboration with Petronas under SEARAH reinforce regional energy security and upstream investment momentum.

Led by the US, Canada and Mexico, North America’s market is driven by midstream expansion, aligning with rising natural gas production and supportive infrastructure policies. Major initiatives such as the Alaska liquefied natural gas export terminal and pipeline by Glenfarne Group and the Alaska Gasline Development Corporation are steadily progressing towards a final investment decision. In the Middle East, upstream activity represents US$358.7bn in CAPEX, dominated by brownfield expansions in Saudi

Arabia, major gas developments in Qatar and the UAE, and offshore exploration in Kuwait.

By Guilherme Bié, OPEX and Decommissioning Analyst and Mariana Messere, Energy Analyst, EIC South America

Image credit | Shutterstock

Follow us

Advertise

Free e-Newsletter