Pipe dream? Beyond the hype and hope of energy transition

There’s a lot of excitement surrounding hydrogen, carbon capture and floating offshore wind, with many projects already on the books. But with the lack of facilities at scale, lack of capacity, lack of demand, lack of policy, lack of funding and lack of profit, Jonathan Dyble asks: are these really net-zero pathways, or simply net-zero pipe dreams?

The case for energy transition is clear:

if we can scale up the capacity of alternative energy sources to improve energy security and affordability, while also moving closer towards net zero, we can solve the ‘energy trilemma’.

However, at present, there appears to be a significant gap between aspiration and actualisation. Do we need to look beyond the hype, slow down and check that the excitement surrounding the energy transition is backed up by reality? It is a serious question that needs to be asked.

At present, the roadmap to scaling up is fraught with challenges. A lack of policies and enabling frameworks, chicken-and-egg dilemmas surrounding supply and demand, uncertainty around financing and profits, and insufficient infrastructure are all blocking the scaling up of key energy transition technologies.

Building a stack of hydrogen plants or carbon capture plants is all well and good. But the reality is, if no one is going to create new demand for hydrogen, or create new markets for carbon, or pay for all the waste products, or provide the tax and regulatory environment for all this to become real, the net-zero journey will come to a depressing halt.

Speaking to industry experts, technology providers and end users, we deep dive into hydrogen, carbon capture and storage (CCS) and floating offshore wind (FOW) to ascertain the size and types of gaps that need to be bridged – and methods for bridging them.

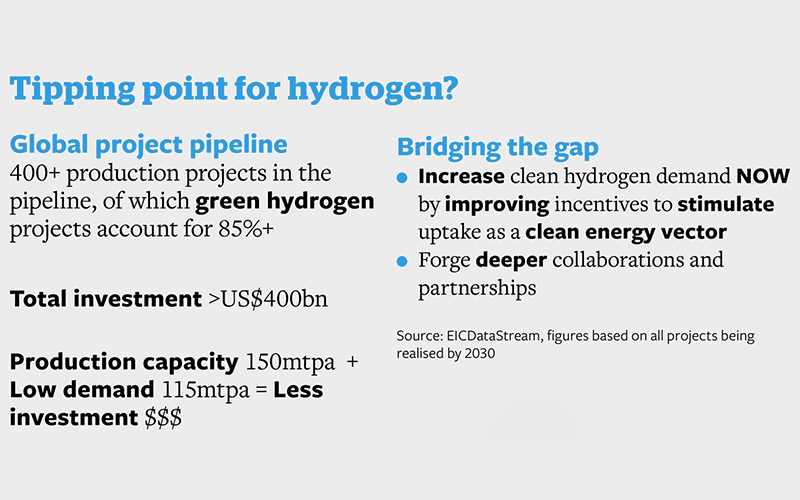

On the face of it, clean hydrogen is a market showing a lot of promise. The global project pipeline currently holds more than 400 hydrogen production projects that are worth about US$400bn in total, with green hydrogen projects accounting for more than 85% of them.

While Europe has historically driven this segment, other regions are now starting to play a greater role. The US, for example, has launched the US$433bn Inflation Reduction Act (IRA), where each kilogram of clean hydrogen is subsidised by the government to the tune of up to US$3. India, meanwhile, has launched its National Hydrogen Mission, committing US$2.3bn to promoting green hydrogen production.

While such initiatives are undoubtedly positive, there are concerns that demand for hydrogen is expected to fall behind production levels by the end of the decade.

“Current hydrogen usage stands at 70 million tonnes per annum (mtpa),” explains Dr Madana Nallappan, Asia-Pacific Regional Analyst at EIC. “If all the projects that have been announced come to fruition by the end of the decade, we will reach a production capacity of 150mtpa. However, projected hydrogen demand for 2030 stands at approximately 115mtpa.”

Interestingly, comments from Nick Wrigley, chairman of end-user First Hydrogen, align with this data. “Major energy players including BP, Shell, Exxon, ENGIE, Total Energies, EDF and INEOS are committing significant investments in the sector, but automotive original equipment manufacturers are reacting more slowly,” he explains. “We believe this is due to their huge commitments to electric mobility, and not a lack of support for hydrogen mobility. However, the single greatest challenge is the creation of distribution networks and publicly available refuelling stations.”

Dr Nallappan adds that we need greater demand stimulus in countries to address the imbalance. “If you are expecting to see demand fall behind production, investors will not be keen to fund new projects,” she explains. “We therefore need to improve incentives on the demand side.”

However, Dr Daniel Chatterjee, Director for Sustainability, Technology Strategy & Regulatory Affairs at Rolls-Royce Power Systems, argues that this has created a chicken-and-egg dynamic, pointing out that neither the use nor the production of hydrogen is established.

“Ramping everything up in parallel – the expansion of renewables, the establishment of a hydrogen ecosystem with production, distribution and use of hydrogen – is difficult,” he says. “We should speed to ramp up, which means simpler and faster permitting processes for renewables, electrolysers and grids and also financial incentives.”

Solving the CCS conundrum

US$125bn of projects slated for 2023–28, but only 2.85% US$3.5bn has reached final investment decision; construction bottlenecks are NOT the cause

Bridging the gap

- Get business models in place

- Carbon pricing frameworks adopted in the long term

- Public investment and subsidies

- Clean energy standards to credit companies generating electricity or other energy sources with CCS

- Global regulation and standards

Carbon capture and storage

In the case of CCS, commitments appear to be similarly buoyant. “Over the two weeks at COP27, we saw a significant number of carbon capture, utilisation and storage [CCUS] announcements, including Saudi Aramco’s plans to develop one of the world’s largest CCUS hubs – with potential storage capacity of 9m tonnes of CO2 a year by 2027,” says Aniruddha Sharma, Chair and CEO of Carbon Clean.

“Heavy industries collectively account for around 30% of CO2 emissions globally. Carbon capture is often the only currently available option for reducing emissions, so it is vital as we transition to net zero. The challenge now is scaling deployment.”

According to EIC data, we could see more than US$125bn of projects move forward between now and 2028. Crucially, however, the value of the projects to reach final investment decision to date has been just US$3.5bn, meaning that of the US$125bn proposed, just 2.85% of the investment has been secured.

“This is not a construction bottleneck – many engineering, procurement and construction companies are ready to break ground,” explains Neil Golding, Director of Market Intelligence at EIC. “Instead, it’s actually a case of getting business models in place to be able to progress those projects.”

Incentives such as the IRA are offering some support here. As a CCS technology provider, Carbon Clean saw US enquiries increase by 64% in the two months following its introduction, for example. However, Golding argues that carbon pricing needs to be adopted in the long term – a viewpoint supported by Bruce Robertson, Energy Finance Analyst at the Institute for Energy Economics and Financial Analysis.

“The policy framework to encourage the transition would be a carbon tax or emissions trading scheme,” he says. “Without a price signal, transition will be slow and ponderous.”

Floating offshore wind

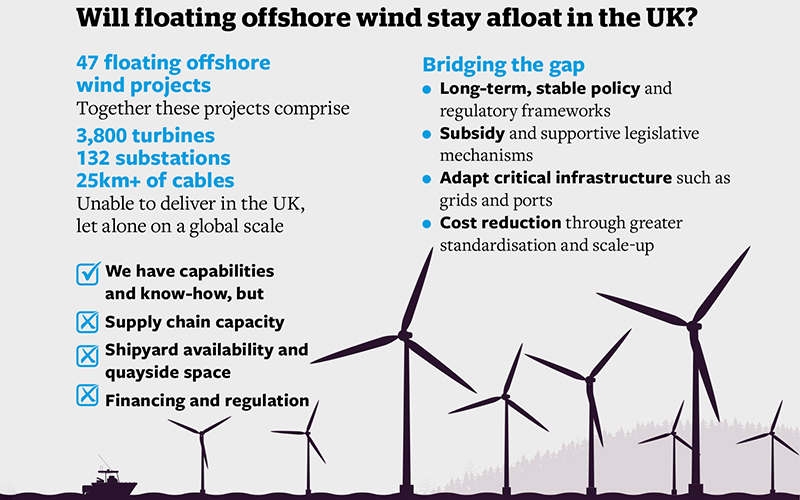

FOW also shows promise, with falling costs improving commercial viability. A wave of opportunities is expected to sweep across the market as a result, with several large-scale commercial developments anticipated to reach final investment decision by 2025–26.

“This is exciting, but it creates issues in terms of how we deliver projects,” Golding explains. “We have capabilities and know-how, thanks to plenty of transferrable skills from oil and gas, but we don’t have the quantity and volume of equipment needed to bring vast numbers of projects to fruition simultaneously.”

He points towards the UK as an example of a major market: it has 47 floating projects in the pipeline that will comprise approximately 3,800 turbines, 132 substations and more than 25km of cables.

“We don’t have the ability to deliver that in the UK, let alone on a global scale,” he says. “Supply chain capacity must expand.”

Success demands a multi-pronged, collaborative strategy

There are undoubtedly reasons to be optimistic about the energy transition. Incentives are improving, driving several large-scale commercial projects towards investment decisions that should serve to expand capacity across hydrogen, CCS and FOW as we move towards the latter half of the 2020s. However, questions remain over whether these markets will boom and accelerate the energy transition quickly enough.

Globally, it is hoped that emissions will be reduced by 45% by 2030, and net zero reached by 2050; energy transition has been hyped up as one of the greatest driving forces towards achieving those critical goals. However, right now, it is hard to find the evidence to prove that will be the case.

Consider the fact that just 2.85% of the investment needed for US$125bn in planned CCS projects has been secured. Consider that we will reach a hydrogen production capacity of 150mtpa in 2030, while projected hydrogen demand will sit lower, at 115mtpa.

“Are there ways that we can reduce installation time for a floating offshore wind farm? For carbon capture, can we look at standardisation to drive capacity increases? Optimisation strategies in these areas will be critical” Neil Golding, Director of Market Intelligence, EIC

This is not to say there is no hope and only hype. There are many underlying issues on both supply and demand side that cast doubt on clean and green energy markets’ ability to take off to the extent needed to make the energy transition. But if the right decisions are made and actions taken quickly, we could see the tide start to turn.

For Aniruddha Sharma of Carbon Clean, policy enhancements such as the setting of clear financial rewards through tax credits or premiums on emissions trading schemes will be crucial. “Governments also need to simplify permitting and planning processes, and put a focus on regulation that supports the growth of a CO2 infrastructure network,” he adds.

In the eyes of EIC’s Neil Golding, cost reduction and standardisation will be critical in unlocking much-needed economies of scale on the development side. He asks: “Are there ways that we can reduce installation time for a floating offshore wind farm? For carbon capture, can we look at standardisation to drive capacity increases? Optimisation strategies in these areas will be critical.”

Furthermore, as well as advocating for demand stimulus, Dr Madana Nallappan highlights the criticality of collaboration. “In the case of hydrogen, aligning hubs and clusters would be a good method for accelerating projects,” she says. “Not only do you reduce risks, but you also reduce the capital that any single company would have to bear, because you have shared infrastructure.”

Between capacity improvements, cost reduction initiatives, improved policy frameworks, greater incentives on both demand and production, and more, there are several hurdles that need to be overcome. However, organisations cannot act alone. Partnerships throughout the value chain will be essential to closing existing gaps between expectation and reality.

Image credit | Shutterstock | Alamy

Follow us

Advertise

Free e-Newsletter