Power sector shifts for coal, gas and carbon capture

From coal-heavy Asia Pacific to gas-driven North America and Europe’s shift toward carbon capture, regional choices reveal the competing pressures of energy demand, security and decarbonisation goals By Aimi Termizi, Research Analyst, EIC kuala lumpur

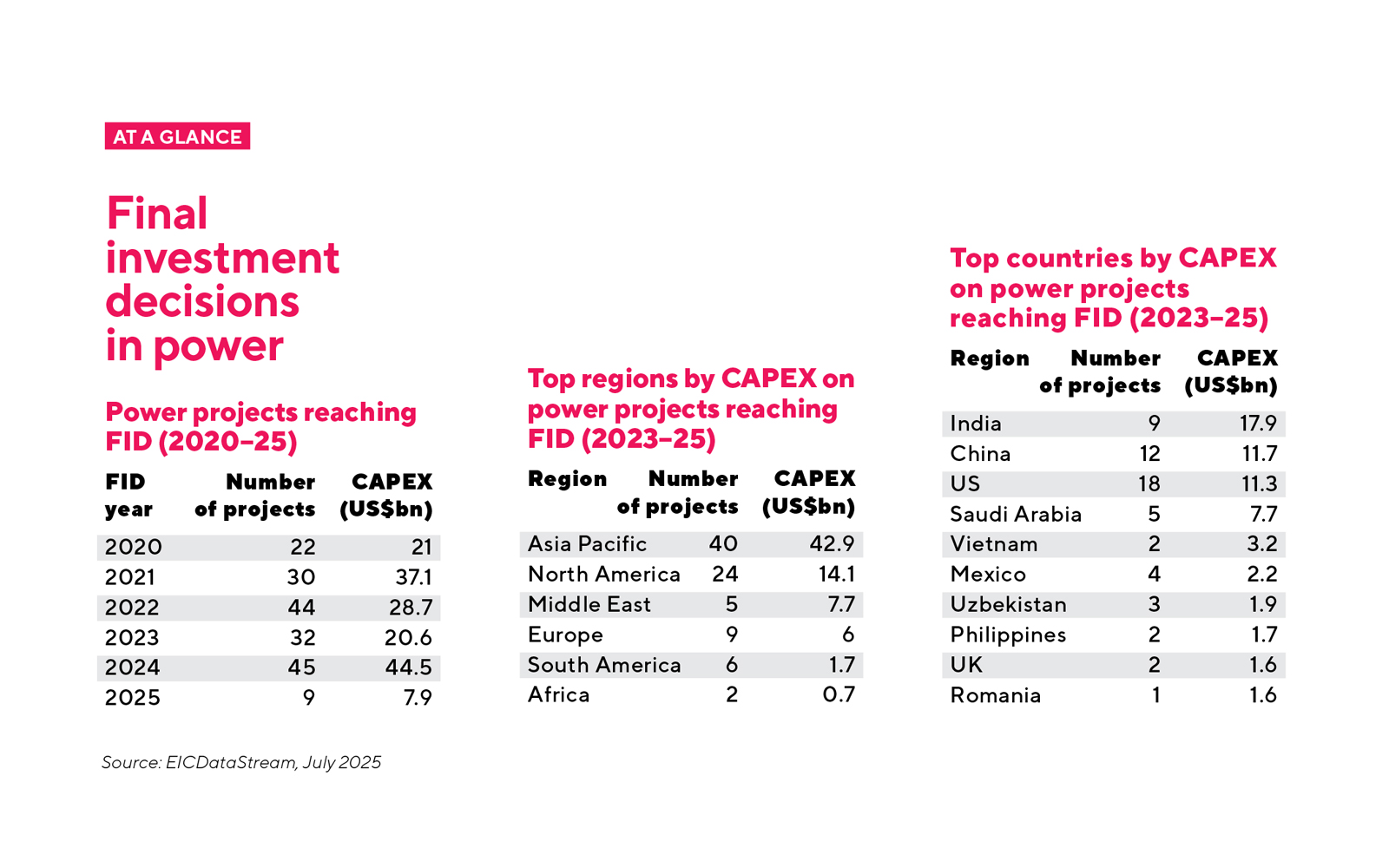

The Asia Pacific region remainsthe global leader in new power projects, recording 28 power projects reaching final investment decision (FID) between 2023 to 2025. These developments represent a total CAPEX of US$31.18bn.

Asia Pacific leads the charge

India stands out as the single largest contributor globally, with nine projectsworth US$17.94bn. India’s high CAPEX is largely driven by significant investment in large-scale coal-fired power plants.

One example is the 800MW Darlipali Coal Power Plant Stage 2, which secured FID in September 2024 with an investment of US$1.27bn. The country continues to depend heavily on coal, which remains the backbone of its electricity generation. The reliance towards coal is largely due to the growing industrial and commercial activity that has significantly increased electricity demand.

To meet the surging demand, the government has instructed power producers to accelerate coal capacity additions, delay retirements and procure US$33bn of additional equipment to maintain and expand coal-based generation until 2030.

The country may increasingly rely on coal plants to offset potential energy deficits, especially during nighttime hours when solar generation drops and during its annual summer monsoon, when wind outputs are lower.

The growing incorporation of CCS technologies is becoming a trend in the power sector, in line with decarbonisation targets

North America’s gas buildout

North America saw 24 projects reach FID between 2023 and 2025, totalling US$14.05bn. The US leads with 18 projects worth US$11.3bn in CAPEX, followed by Mexico with four projects worth US$2.15bn.

Most of these projects are gas-fired developments, particularly combined-cycle gas turbine plants, reflecting both the need for grid flexibility and the gradual retirement of coal units. While gas-fired power plants do not directly qualify for renewable generation tax credits, the Inflation Reduction Act offers indirect benefits that can enhance project viability.

Gas-fired power plants that integrate carbon capture and storage (CCS) can qualify for the 45Q tax credit. Moreover, surging electricity demand from technology sectors including data centres and the abundance of domestic natural gas are expected to sustain the region’s gas buildout in the near term.

Europe focuses on carbon capture

Europe has nine power projects moving forward, with a total CAPEX of US$6.04bn. The growing incorporation of CCS technologies is becoming a trend in the power sector, in line with decarbonisation targets. Many new gas-fired power projects are being developed with integrated CCS capabilities, and several existing plants are being retrofitted to reduce emissions while maintaining grid reliability.

Notably, the UK’s Net Zero Teesside Power project, part of the East Coast Cluster, reached FID in December 2024. The project will generate up to 742MW of electricity from natural gas and will have CCS technologies incorporated on site.

While Europe ranks third globally in terms of number of projects reaching FID, the region continues to face hurdles such as complex permitting procedures, high regulatory standards and slower approval timelines that may affect project execution.

ARE YOU READY TO EXPORT? Email: aimi.termizi@the-eic.com

Image credit | iStock

Follow us

Advertise

Free e-Newsletter