Slow burn, bright prospects: opportunities on the horizon for hydrogen and carbon capture

Advances in the hydrogen and carbon capture energy sectors have been slow, but opportunities exist in Europe, Australia and the US, says Fernando Vieira at EIC.

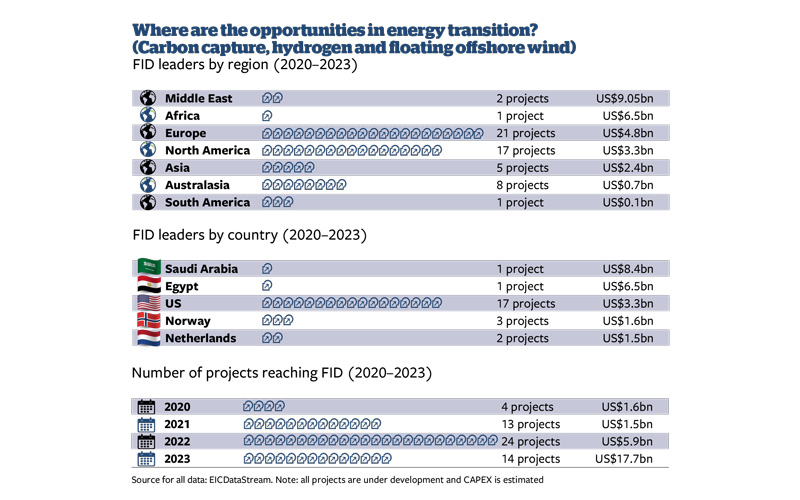

Since 2018, the global energy sector has seen a surge in announcements of carbon capture and storage (CCS) and clean hydrogen projects. While this is a positive trend, most of these projects are still in their early stages, presenting challenges when it comes to transitioning from feasibility plans to operational assets. For these projects to contribute significantly to net-zero objectives, critical gaps must be addressed, such as the scale-up of CCS and hydrogen supply chain technologies, seamless integration into existing energy grids, and the establishment of storage and distribution infrastructure.

While global funding programmes and subsidies are aiming to enhance the commercial scalability of technologies and drive profitability, markets in Europe, Australia and the US are attracting investors due to their coherent legal frameworks and highly appealing long-term supply contracts.

Europe’s green energy drive

Norway and the Netherlands are actively advancing their substantial CCS initiatives. Having reached a final investment decision (FID) in October 2023, the Netherlands’ Porthos CCS project, with a US$1.37bn investment, aims to be operational by 2026. Meanwhile, Norway’s Northern Lights project, set to begin operations in 2024, will handle 1.5m tonnes of CO2 annually. The US$4.5bn Heidelberg Cement Plant in Brevik also secured FID in December 2020. Both projects will contribute to Norway’s Longship initiative, which aims to establish a complete CCS value chain throughout the country by 2024.

Meanwhile, hydrogen and CCS are poised for growth in the UK, the Iberian Peninsula and Denmark. bp’s US$1.2bn H2Teesside project in the UK, which focuses on blue hydrogen production from natural gas, is a standout initiative; an FID is expected by late 2024 and start-up by 2029. Also in the UK, Kellas Midstream’s H2NorthEast project, a US$1.6bn low-carbon blue hydrogen facility, is in the front-end engineering and design (FEED) stage; an FID is anticipated by mid-2025.

In the UK, the CCS and carbon capture, utilisation and storage (CCUS) sectors aim to decarbonise industrial clusters, with notable projects including H2Teesside Carbon Capture, H2NorthEast Teesside Carbon Capture and Stanlow Refinery CCS. The latter secured a pre-FEED contract in late 2022 and targets a a start-up date of 2028, with the FID anticipated by late 2024.

Scotland’s Stratera is developing the Kintore Green Hydrogen Plant, a US$500m project that aims to produce 200,000 tonnes of green hydrogen annually. The FEED contract, awarded to Worley, is targeted for completion in Q4 2024, followed by an FID in 2025.

Portugal’s Madoqua project, a US$1bn green hydrogen and ammonia production venture in Sines led by Power2X, is expected to begin operations in 2027; an FID is anticipated by mid-2025. Galp’s US$264m green hydrogen plant, also in Sines, aims to begin operations in 2025 after an FID in September, contracting Plug Power for electrolysers and Technip Energies for overall engineering, procurement, construction and management.

FIDs for Spain’s Catalina project (US$1.7bn) and Denmark’s Esbjerg Green Hydrogen project (US$3bn) are anticipated in late 2024 and mid-2024 respectively. Copenhagen Infrastructure Partners is developing the Spanish project, with Technicas Reunidas as the FEED contractor. Meanwhile, Trafigura will develop the Danish project, with Plug Power supplying the electrolysers and Ramboll handling the project management contract.

North America strategically positions for domestic and international supply

The Louisiana Clean Energy Complex in Ascension Parish, Louisiana, is poised to be a significant player, producing more than 750m cubic feet of blue hydrogen per day, with CO2 capture for permanent sequestration. Securing a substantial US$7bn FID in November 2023, this boost in funding is credited to the Inflation Reduction Act passed in August 2022, which is driving investments in renewables. MAN Energy Solutions and Baker Hughes are on board to provide essential equipment and technology.

ExxonMobil’s US$2bn Baytown Blue Hydrogen and CCS Project in Texas has also advanced, with the FEED phase contract awarded to Technip. With an FID anticipated in June 2024, the project is set to start producing blue hydrogen in 2028.

In the Middle East, Saudi Arabia and Oman are at the forefront of decarbonisation initiatives within their oil and gas sectors

Three carbon capture projects are awaiting FIDs, including the Baytown CCS Project and the Tundra CCS project in North Dakota. The latter aims to capture 90% of CO2 emissions from a coal-based power plant, with Fluor Corporation handling the FEED and Kiewit overseeing construction. An FID is targeted for late 2024, and start-up for 2026.

Australia’s promising market

Australia is poised to be a key player in the burgeoning green hydrogen sector, boasting a substantial pipeline of projects with significant CAPEX and production capacity. It aims to become a leading net exporter of low-emissions hydrogen by 2030 and the largest by 2050, according to the International Energy Agency’s 2022 World Energy Outlook.

Notable projects include the Aldoga Green Hydrogen Plant in Queensland, a U$1bn initiative by Iwatani with an FID expected in late 2024. This project strategically explores export opportunities, particularly to the Japanese market. In Western Australia, plans are underway for a U$3bn Green Hydrogen Plant in Murchison, set to start construction in 2025 and begin operations in 2030.

In the CCS market, the Bayu-Undan Carbon Capture and Storage Project in the Timor Sea is estimated at US$1.1bn and expected to start operations in 2026, pending an FID around late 2024 or early 2025. Worley has secured a FEED contract for the project’s offshore facilities and pipelines.

The Middle East’s decarbonisation drive

In the Middle East, Saudi Arabia and Oman are at the forefront of decarbonisation initiatives within their oil and gas sectors. NEOM and ACWA Power in Saudi Arabia are creating a US$8.4bn Green Hydrogen Plant in Tabuk Province, using 4GW of solar and wind power to produce 650 tonnes of green hydrogen daily. Slated to start in late 2026 following a May 2023 FID, the project will leverage thyssenkrupp technology.

Saudi Aramco is spearheading the development of the world’s largest CCS hub: the US$4.5bn Jubail Industrial City project, expected to be operational by 2027. Meanwhile, Oman is planning a green ammonia and hydrogen facility in the Duqm Industrial Zone, which will use 3GW of solar and 500MW of wind power to yield 1.2m metric tonnes of green ammonia daily. ACME Solar is set to make an FID in late 2025, with start-up anticipated by 2027.

Furthermore, a US$1bn green hydrogen and ammonia project in the Salalah Free Zone is undergoing feasibility studies. It aims to generate 400MW of green hydrogen and 365,000 tonnes of green ammonia annually from 3.8GW of wind and solar energy. Developer OQ anticipates an FID by mid-2024.

Five major projects targeting FID in 2024/2025

Acorn CCS Transportation & Storage Project

- Value: US$9bn

- Country: Scotland

- Operator: Storegga

- Start-up year: 2027

Pecém Port Green Hydrogen Plant

- Value: US$6bn

- Country: Brazil

- Operator: Fortescue Metals Group

- Start-up year: 2027

St. Rose Blue Ammonia Plant

- Value: US$4.6bn

- Country: US

- Operator: St. Charles Clean Fuels

- Start-up year: 2027

Summit Carbon Solutions CCS Project

- Value: US$4.5bn

- Country: US

- Operator: Summit Carbon Solutions

- Start-up year: 2026

Duqm Green Ammonia & Hydrogen Project

- Value: US$3.5bn

- Country: Oman

- Operator: ACME Solar

- Start-up year: 2027

By Fernando Vieira, Energy Consultant, EIC.

Interested in exploring energy transition opportunities?

Inform your decision-making with the latest contracting activity and markest research from EIC. To discuss your needs, email Aadam Sufi at Aadam.Sufi@the-eic.com

Image credit | Shutterstock | Getty

Follow us

Advertise

Free e-Newsletter