Are we ready to rise? From chaos to clarity - building a world that works

The global energy transition encountered significant headwinds in 2024, from policy uncertainty to capital constraints. As the industry seeks to regain momentum, Tom Wadlow explores how setbacks can be turned into opportunities for a more sustainable future.

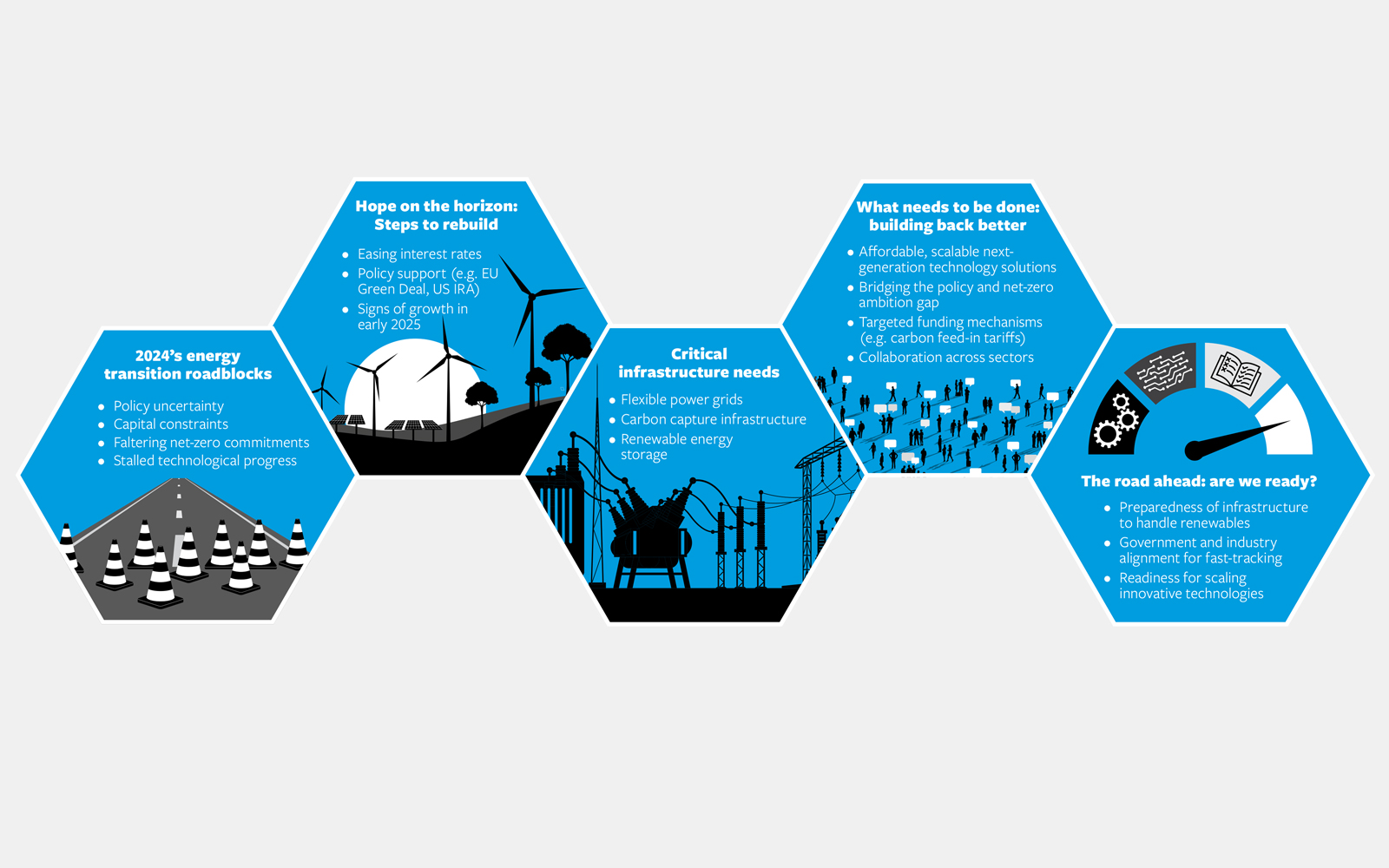

The energy transition narrative of 2024 reads somewhat like a cautionary tale.

From faltering net-zero commitments to stalled technological progress, the sector faced unprecedented challenges that threatened to derail decades of progress. Yet within these setbacks lie crucial lessons that could help forge a more resilient path forward.

Juliet Davenport is a climate scientist and renewable pioneer whose contribution to climate action spans more than two decades. After achieving degrees in physics and economics, in 2000 she founded the UK’s first 100% renewable electricity supplier, Good Energy, which she successfully led to an AIM listing in 2012. Having served as President at the Energy Institute, last year she was chosen to advise the UK Government’s Department for Energy Security and Net Zero on delivering its Clean Power 2030 Mission.

Davenport calls 2024 “a challenging year for global innovation investment in the energy transition”, adding: “High interest rates have made long-term investments more expensive, as evidenced by listed renewable funds trading below net asset value and struggling to secure capital.”

Capital constraints and market confidence

The financial headwinds have been particularly severe. Matthew Taylor, Managing Director of Green Giraffe Advisory, points to the cost of capital as the fundamental challenge.

Everyone wants a net-zero future, but it must be affordable now. We must invest in next-generation technologies that lower the cost of decarbonisation Tom White, C-Capture

“Capital is the fuel of the energy transition and the dramatic increase in rates has thrown cold water on the commercial viability of a number of segments within the energy transition,” he says. “In turn, for many, there’s been a retreat to core markets and technologies which has, to some extent, stifled deployment of new technology.”

This retreat has hit innovative startups particularly hard. Tom White, CEO of carbon capture technology developer C-Capture, has experienced these challenges firsthand.

“The broader investment landscape for pre-revenue companies has hit a five-year low,” he explains. “A lack of timely market signals to implement government policy has eroded investor confidence in revenue forecasts.”

Indeed, C-Capture’s situation exemplifies the precarious position that many innovative energy transition companies find themselves in. Despite achieving its strongest technical year to date, with a successful demonstration of its technology on a third prototype pilot plant and independent verification of major technical objectives, C-Capture faces an existential challenge.

2024 has proven to be a challenging year… High interest rates have made long-term investments more expensive, as evidenced by listed renewable funds trading below net asset value and struggling to secure capital Juliet Davenport, UK Energy expert

“We are now ready for the next stage – building £50–100m worth of infrastructure for a first-of-a-kind commercial-scale prototype,” White continues. “However, this falls outside the investment scope of most climate venture capitalists and is not yet de-risked enough to attract infrastructure investors.”

The stakes are high. Without securing a buyer with the necessary vision and funding, the company may need to enter what White calls ‘Sleeping Beauty mode’ – mothballing physical assets and documenting technology in the hope that a future owner can revive the project when market conditions improve. This scenario would not only affect C-Capture’s staff, all of whom are now on notice, but also delay crucial carbon capture innovation at a time when such technologies are badly needed.

Building back better

Despite these challenges, industry leaders, including White, do see the potential for recovery in 2025.

Davenport identifies several reasons for cautious optimism, including the potential easing of interest rates and stronger policy support through initiatives such as the EU Green Deal Industrial Plan and US Inflation Reduction Act.

“It is too early to say if 2024 was the bottom of the cycle,” Taylor adds. “In early 2025, we have seen tentative signs of an uptick in project development cadence and in M&A activity. Some of this is supported by fundamentals like the gradual lowering of interest rates.”

However, rebuilding momentum requires more than just improved financial conditions. Indeed, there are calls for a fundamental reset in the way the energy transition is approached.

White emphasises the importance of making sustainable solutions economically viable. “Everyone wants a net-zero future, but it must be affordable now,” he says. “We must invest in next-generation technologies that lower the cost of decarbonisation.”

Bridging the policy gap

The disconnect between ambitious climate targets and practical implementation remains a critical challenge.

“We’ve had a lot of targets set,” Taylor observes. “It helps to set long-term expectations, which enables business to assess the scale of the opportunity. However, there is clearly a mismatch between these targets and the scale of deployment, particularly in wind.”

One of the major observations Davenport has made in her work in the energy transition field is the importance of transparent communication between stakeholders.

“There are inherent communication challenges between industry, policymakers and consumers,” she says. “Each group has different priorities and incentives, which can create tension or a disconnect in how the energy transition is approached.”

It is too early to say if 2024 was the bottom of the cycle. In early 2025, we have seen tentative signs of an uptick in project development cadence and in M&A activity Matthew Taylor, Green Giraffe Advisory

The path forward therefore requires striking a delicate balance between maintaining ambitious climate goals and ensuring practical implementation.

But the need for balance cannot be used as an excuse to slow down action. For companies such as C-Capture, seeking to blaze a trail for the transition to net zero, time is of the essence. “I wouldn’t say policymaking is out of sync with reality, but the process is simply too slow,” says White. “It takes too long for policies to become law, for mechanisms to be translated into revenue support, and for final investment decisions to be made on key projects.”

Is infrastructure the biggest hurdle?

One important element in rebuilding momentum will be developing robust infrastructure to support the energy transition. As renewable energy penetration increases, the need for flexible, resilient systems becomes paramount.

“As the percentage of renewable energy on power grids continues to rise worldwide, managing the variability of their output will become increasingly critical,” Davenport explains. “The need for flexibility will grow across various sectors, from domestic flexibility using home heating systems and electric vehicle chargers to industrial flexibility, where large-scale facilities can adjust their energy consumption based on supply and demand.”

This infrastructure challenge extends beyond just power generation and distribution. The success of innovative technologies such as carbon capture also depends on having the right supporting systems in place.

“What we currently lack is a clear and transparent timeline for when industrial sequestration infrastructure will be built,” White notes. “Only when that infrastructure is in place can developmental technologies plan for implementation and generate revenue, providing a clear path to return on investment.”

The investment required for such infrastructure development is substantial, particularly given current market conditions. Taylor emphasises that while long-term growth is important, it is not critical in the short-to-medium term because there is a lot of conventional power that needs to be replaced. That said, he warns that cost of capital and inflation are critical, particularly now that the prevalence of centrally reported revenue models is reducing.

Looking at the UK specifically, progress has been mixed. “While the country is a leader in offshore wind energy, with ambitious goals for wind capacity expansion, managing the variability of renewable energy output remains a key challenge,” Davenport observes. “The transition to a more flexible grid is happening, but the current infrastructure and systems are often viewed as not yet fully capable of handling the dynamic, decentralised energy flows that will come with a greater share of renewables.”

Creating an enabling environment

The path forward requires not just technological innovation, but also new approaches to funding and implementing these solutions.

For example, White advocates for targeted support mechanisms, such as a carbon feed-in tariff: “A carbon feed-in tariff of £100–200 per tonne would be transformational,” he says. “It would support early revenues for first-of-a-kind technology demonstrations, reduce CO₂ costs for UK consumers, improve security of supply, and kickstart a UK engineering supply chain for next-generation carbon capture modules.”

As the industry looks to 2025 and beyond, the focus must shift from setting targets to creating conditions that enable their achievement.

This means investing in new technologies as well as building the infrastructure, policy frameworks and market mechanisms needed to support them. Only through a joined-up approach can the setbacks of 2024 be transformed into a foundation for a more sustainable and resilient energy future. The burning question now is: are we ready to rise to the occasion?

A view from Aberdeen

As Chief Executive of the Aberdeen and Grampian Chamber of Commerce (AGCC), Russell Borthwick represents the interests of 1,300 companies collectively employing more than 100,000 people. With around a third of its members operating in the energy supply chain, the AGCC represents a region at the heart of the UK’s energy sector. The city is also set to host the UK government’s new GB Energy organisation, tasked with driving clean energy deployment.

For Borthwick, the current energy transition discourse needs refinement. “The energy transition debate needs to mature because, at the moment, it is too polarised,” he explains. “Transition means change over time, and our concern is that the decline of the North Sea oil and gas industry is accelerating before enough scalable and bankable renewable energy projects come into play.”

The region faces a critical challenge in retaining its expertise. “Aberdeen and our region are home to the world’s best energy supply chain and talent,” Borthwick notes. “What our member companies need is profitable and secure projects to work on, and at the moment, they are being forced to take on work overseas. This exodus of talent and resources could undermine the UK’s clean energy ambitions.”

While acknowledging the imperative to decarbonise, Borthwick questions the proposed timeline. Currently, oil and gas accounts for around 75% of UK energy use, and even by 2050 and the net-zero scenario, the government’s own Climate Change Committee acknowledges that gas, in particular, will still be part of the energy mix. The UK’s increasing reliance on gas imports – projected to reach 80% by 2030 – raises additional environmental concerns, as imported LNG brings with it a carbon footprint more than four times greater than that of domestically sourced supply.

For Aberdeen, the opportunity is clear but depends on careful management of the transition. “If we get the pace of the transition right,” Borthwick says, “there is massive potential for the North East of Scotland to become the UK’s clean energy hub.”

Image credit | ADOBE ILLUSTRATOR AI | iStock | Shutterstock

Follow us

Advertise

Free e-Newsletter