Push for offshore wind gathers pace after setbacks

Supply chain pressures, policy uncertainty and stalled pipelines have slowed offshore wind. But across Europe, Asia Pacific and South America, fresh reforms and auctions are reviving momentum — though risks remain By Hazwani Izzati, Energy Analyst, Eic Kuala Lumpur

Wind farm at Icaraizinho, Brazil

The offshore wind industry has faced significant challenges in the last few years, including project cancellations, delays, poor auction interests and developers exiting new markets – driven largely by macroeconomic headwinds and supply chain bottlenecks. Europe has been particularly affected, yet the region, led by the UK, Germany and the Netherlands, continues to hold its position as a global leader in the sector.

Europe: Still leading through reforms

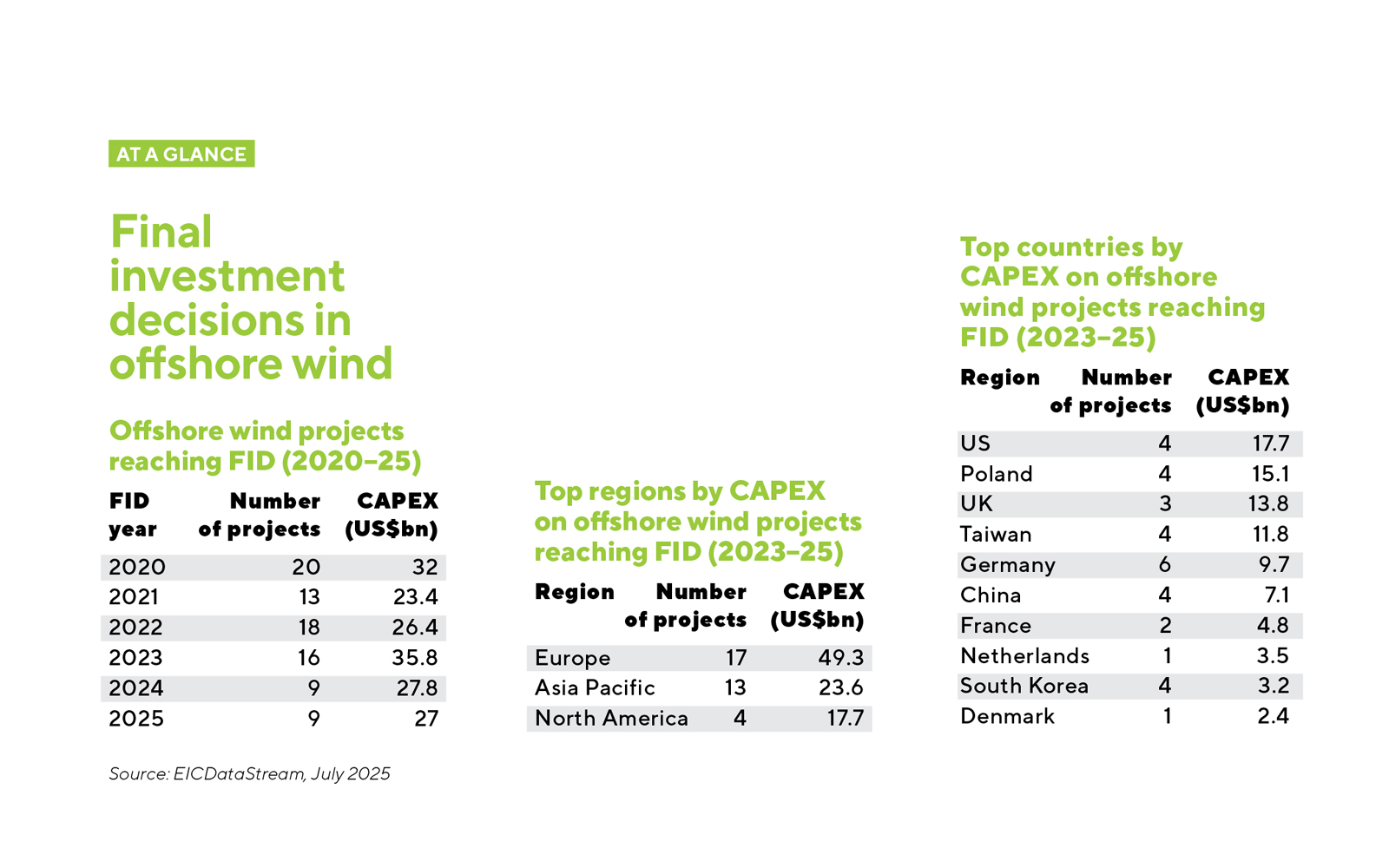

Since 2023, the region has seen 17 projects reach final investment decision (FID), amounting to US$49.32bn. FID activity has doubled in 2025 compared to 2024, supported by policy and auction reforms aimed at addressing the challenges. The UK is expected to add the most capacity, targeting 29GW of fixed-bottom wind by 2030 and 29.57GW by 2035 for floating technology – but further project delays are anticipated.

So far, three fixed-bottom projects, totalling 5.33GW and worth US$13.84bn, have reached FID. The region is focusing on policy changes to mitigate ongoing challenges. In the UK, eligible fixed-bottom projects can now participate in the 2025 Allocation Round 7 Contracts for Difference (CfD) subsidy auction without prior planning consent – with test and demonstration-scale floating wind projects now allowed to join. The CfD contract has also been extended from 15 years to 20 years for both technologies.

Strong momentum in South Korea and Taiwan

The Asia Pacific region (excluding China) has seen active developments, particularly in South Korea and Taiwan. A total of 13 projects have reached FID, totalling US$23.12bn.

South Korea leads, with 6.79GW of fixed-bottom offshore wind expected to come online by 2030 and 13.25GW of floating wind by 2035 (subject to industry challenges). Four fixed-bottom projects totalling 889MW have reached FID, with a CAPEX of US$2.7bn.

Taiwan follows close behind, with 6.42GW of fixed-bottom offshore wind by 2030 and 12.87GW of floating wind by 2035. Four projects, totalling 2.44GW and worth US$11.8bn, have reached FID.

The region is moving forward with upcoming offshore wind auctions. South Korea’s H1 2025 auction currently has six bidders participating, while Taiwan has opened consultations for its Round 3.3 auction, proposing up to 3GW of new capacity. Australia, while still emerging, is expected to have one of the largest offshore wind pipelines in the long term, with its first auction in Victoria in September 2025.

Offshore wind in South America is still in its early stages, but the region holds significant potential to shape the future global pipeline

South America: Emerging market, big potential

Offshore wind in South America is still in its early stages, but the region holds significant potential to shape the future global pipeline. Brazil leads the region, with 95 proposed projects, which have a total estimated capacity of 225.82GW.

Progress had been uncertain, as regulatory gaps made it unclear which projects could go ahead. However, this changed with Brazil’s 2025 Offshore Wind Law, which enacted a legal framework for offshore wind development. The country’s first sea use concession auction is expected in Q4 2025, opening the way for developers to obtain environmental licenses and begin feasibility studies.

Colombia is also advancing in this area, with its first offshore wind auction underway. The Colombian government has received 69 site nominations for potential development in this auction, focusing on the Caribbean coast. It aims to award 1GW by August 2025, with a minimum project size of 200MW.

Policy uncertainty in North America

Although the US leads the North American region with 5GW having reached FID since 2023, recent policy shifts under Trump have introduced uncertainty. These include cuts to clean energy tax credits and stricter development requirements, casting doubt on the future of its offshore wind pipeline.

Are you ready to export? Email: hazwani.izzati@the-eic.com

Follow us

Advertise

Free e-Newsletter