Transition technologies face development hurdles

Policy gaps, funding and inflation are hindering progress for hydrogen, sustainable aviation fuel and floating offshore wind projects, says Nabil Ahmed

The transition to cleaner energy relies heavily on emerging technologies such as hydrogen, sustainable aviation fuel (SAF) and floating offshore wind. These innovations promise to decarbonise hard-to-abate sectors, but despite a growing pipeline of projects, escalating challenges – inflation, policy gaps and funding constraints – are stalling critical projects, putting the global energy transition at risk.

Headwinds for hydrogen projects

Green hydrogen, produced from renewable energy, offers a clean energy storage solution and complements intermittent renewables such as solar and wind, reducing reliance on fossil fuels. However, the industry is grappling with delays caused by weak demand, insufficient infrastructure, inadequate policy frameworks and weak financial drivers.

Uniper’s large 100MW H2Maasvlakte project in the Netherlands exemplifies this struggle. Due to the failure of securing a power purchase agreement, its full-scale development has been scaled back and delayed to 2030; only one-fifth of its capacity is expected by 2028.

Similarly, Repsol in Spain has put several renewable hydrogen investments on hold because of the local government’s plan to make permanent its windfall tax on energy revenues. As such, the developer has decided to only go forward with one project in its pipeline.

The situation in the US is no different. Hy Stor Energy has terminated its agreement for 1GW of electrolyser capacity with Nel for an undisclosed reason. The Mississippi Clean Hydrogen Hub project was poised to be the largest off-grid hydrogen production and salt cavern storage hub in the US.

SAF struggles to take off

As the aviation sector aims to decarbonise, SAF – a low-carbon alternative to conventional jet fuel – will become increasingly important as the only viable near-term option, reducing lifecycle emissions by up to 80%. However, costs remain prohibitive; SAF production can be five times costlier than traditional jet fuel, creating hesitation among investors.

Setbacks have plagued major SAF projects. In the UK, Velocys’ Altalto SAF plant is stuck in its pre-construction phase with no clear timeline for a final investment decision (FID). This may be down to factors such as insufficient funding (despite the availability of subsidy mechanisms) and prolonged front-end engineering design studies due to the nascency of the technologies – challenges that exist in many other projects.

Projects are also struggling to secure the investment needed to reach the construction stage. In the US, developer Gevo has been working for almost 12 months to secure a loan guarantee from the US Department of Energy to fund the construction of the Net Zero 1 SAF project. This hold up has set the project back by more than a year.

The SAF sector’s shift towards hydrogen-powered power-to-liquid processes adds complexity, with investors hesitant about the high costs in such a novel industry. The financial returns, on paper, do not appear to justify the investment. Without government-mandated strategies and robust incentives, private sector confidence is unlikely to grow.

Rough waters for floating offshore wind

Floating offshore wind technology unlocks wind energy potential in deeper waters where fixed turbines are not viable. It boosts renewable energy capacity significantly, particularly for nations with deep coastal areas, contributing to global renewable energy goals. However, progress is hampered by financial and logistical hurdles.

In the UK, Blue Gem’s Erebus offshore wind farm failed to secure a Contract for Difference, preventing the project from moving forward. Developers have indicated that without adequate funding, floating offshore wind projects cannot proceed. Furthermore, delays and challenges in established markets emphasise that these issues are not confined to newer or less experienced regions.

Floating offshore wind is struggling to progress due to several challenges that have yet to be resolved for fixed-bottom turbines, including port and vessel availability and manufacturing limitations. With fixed-bottom projects already encountering physical and logistical hurdles, many companies are reluctant to invest in floating offshore wind until these matters are resolved.

Inflation and supply chain woes

Across all three technologies, inflation has squeezed developers and supply chains alike. Rising costs make it difficult to achieve profitability, leading companies to deprioritise energy transition projects in favour of ventures such as oil, gas and nuclear.

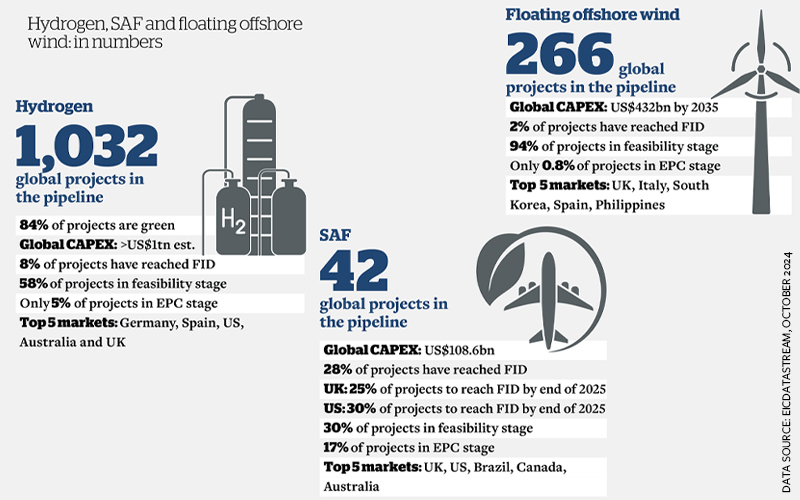

According to EICDataStream, energy transition FID rates are starkly low: only 8% of hydrogen, 28% of SAF and 2% of floating wind projects globally have reached FID as of September 2024. This trend reflects the broader uncertainty and financial constraints affecting these nascent sectors.

Bridging gaps with policy and support

While hydrogen, SAF and floating offshore wind all have substantial project pipelines that present opportunities for the supply chain, the industry has yet to see a significant number of projects reach FID and achieve the milestones necessary for commercialisation to truly take off.

To unlock their full potential, governments and stakeholders must address these systemic challenges through targeted policies, robust funding mechanisms, and incentives to attract investment.

Failure to act risks stalling the energy transition at a time when the world cannot afford to fall behind.

By Nabil Ahmed, Energy Analyst at EIC

Image credit | Getty

Follow us

Advertise

Free e-Newsletter